Do we actually know where will the world be after 6 months? As the Corona Virus pandemic gradually spreads its claws all over the world, we are trying hard, joining hands, trying to fight the destruction to make the mother earth sustainable. We are maintaining social distancing and lockdown to tackle the ill effects of the virus; the businesses have pressed the pause button and the whole economy is witnessing a downfall. The stock markets were the first in the line to get affected. The travel industry has been massively hit since there were restrictions in travel and gradually it has put a check in the domestic and international travel, although the supermarkets and the online groceries have witnessed a high demand due to the social distancing and the lockdown. Immediately after the outbreak, people had been piling groceries at their home. There has been a major drop in the air pollution post the lockdown and we could see the nature dancing in its own rhythm.

Although the lockdown resulted in a halt in the manufacturing and production chain all round the world, but it is likely that the countries like India, with cheap labour will climb the ladder and end up starting inhouse manufacturing and exports. According to Customs statistics, China’s foreign trade volume in 2019 stood at RMB31.54 trillion, up by 3.4% year-on-year (similarly hereinafter). Exports rose by 5% to RMB17.23 trillion and imports grew by 1.6% to RMB14.31 trillion. The trade surplus increased by 25.4% to RMB 2.92 trillion. In 2019, China’s foreign trade registered a momentum of improving quality amid overall stability. The People’s Republic of China shipped US$2.499 trillion worth of goods around the globe in 2019 along with its various other partner countries. As per the latest available data, it may be seen that approx. 60.2% of products were exported from China and bought by importers in: the United States (16.8% of the global total), Hong Kong (11.2%), Japan (5.7%), South Korea (4.4%), Vietnam (3.9%), Germany (3.2%), India (3.0%), Netherlands (3%), United Kingdom (2.5%), Taiwan (2.2%), Singapore (also 2.2%) and Malaysia (2.1%). With the closing down of the manufacturing and distribution units in China there has been a major drift and scarcity of the imported products and the small scale distribution channels. China posted a $295.8 billion trade surplus with the United States in 2019.

With the major halt in the exports by China, there is a sudden shortage of supply of various products like Phone system devices including smartphones, Computers, optical readers, Integrated circuits/micro assemblies, Processed petroleum oils, Solar power diodes/semi-conductors, Automobile parts/accessories, Lamps, lighting, illuminated signs, Computer parts, accessories, Models, puzzles, miscellaneous toys and TV receivers/monitors/projectors market all over the world.

What’s coming next?

In order to save the entrepreneurs and the industry in this crisis, the Indian Government has been taking certain steps to:

A. Prevent the opportunistic takeovers of the Indian businesses; and

B. Make a conducive environment to make India a global manufacturing hub

The above may be described in details.

A. Prevent the opportunistic takeovers of the Indian businesses:

Check post on the Foreign Direct Investment (FDI):

On April 18, 2020, the Department for Promotion of Industry and Internal Trade (DPIIT) issued its Press Note 3 of 2020 (PN 3 of 2020 Series) whereby they have reviewed the current Foreign Direct Investment (FDI) Policy and has brought in major changes in the policy in order to prevent opportunistic takeovers/acquisitions of the Indian companies due to the current COVID-19 pandemic. According to the release,

“A non-resident entity can invest in India, subject to the FDI Policy except in those sectors/activities which are prohibited. However, an entity of a country, which shares land border with India or where the beneficial owner of an investment into India is situated in or is a citizen of any such country, can invest only under the Government

route. Further, a citizen of Pakistan or an entity incorporated in Pakistan can invest, only under the Government route, in sectors/activities other than defence, space, atomic energy and sectors/activities prohibited for foreign investment.”

Countries sharing land borders with India are Pakistan, Bangladesh, China, Nepal Bhutan and Afganistan. Hence by this Press Note, the Department has allowed both direct and indirect investment in India by any entity or beneficial owner or citizen of that country ONLY by way of Government Approval. The Press Note further says that if there is any transfer of ownership of any existing or future FDI in an entity in India, directly or indirectly, resulting in the beneficial ownership falling within the aforesaid restriction/purview, such subsequent change in beneficial ownership will also require Government approval. The primary intent of the Department is to regulate any attempts by Chinese entities/ beneficial owners/citizens to take control of Indian entities which have been affected by COVID-19 lockdowns. Now, fresh infusion of funds by Chinese entities in existing investments in India would also require government approval. The Department is even putting the restrictions on the multi-layered structures, spread across various jurisdictions.

Subsequently, the Securities and Exchange Board of India (SEBI) has issued directives to the custodians for the FPI investments or beneficial interest information of investors coming from China as well as Hong Kong. It is now scanning the hubs such as the Cayman Islands, Singapore, Ireland and Luxembourg to track the direct and indirect investments from China and Hong Kong in the country.

It has been mentioned that the intent of the Department is to curb opportunistic takeovers/acquisitions of the Indian companies due to the current COVID-19 pandemic. Deep down it can be said that post the HDFC Ltd. disclosure on April, 11, 2020, that the China’s central bank People’s Bank of China (PBoC) has increased its stake in the Company from 0.8% to 1.01%, the Department and SEBI has been minutely watching the FDI movement in the country.

B.Make a conducive environment to make India a global manufacturing hub:

i. India the next manufacturing hub:

The effects of the recent lockdown in China were felt by many Japanese, Korean and other manufacturers which witnessed the supply of components for their factories grind to a halt since factories in China shuttered. Now, various companies are planning to shift its manufacturing units from China to the different other Asian states. Countries like Japan are in talk with the Indian Government to set up their base in India. Market giants like Google, Microsoft, Apple are even planning to move out of China and set up their manufacturing units in countries like Vietnam, Thailand etc.

India will be a very good choice for these companies due to its extremely cheap labour cost, maximum workforce base, favorable diversified weather conditions and huge area in the country.

ii. Self reliant:

As a result of the complete shut down of the economic activity, India along with other countries is expected to face a downfall in the GDP in the 1st quarter of the Financial Year 2020-21. Although from the second and third quarters, it is expected to witness a steady growth with the increase in in-house manufacturing and supply as per the market demand. There is ample opportunity for the SMEs in India to regularize the global supply chain disruption caused by the outbreak of the pandemic COVID-19. India has less dependence on China for the intermediate goods and with the added factor of cheap labour and lower manufacturing cost, the manufacturing sector will see a boom in its growth history. India can easily manufacture the various consumer products and export both the raw materials and the finished products in large scale.

iii. Employment Generation and Government support:

Although the sector wise production is expected to decrease in the recent times, but there is huge scope of employment generation in the coming days. The Indian Government has been reviewing its policies in order to combat this crisis and have even come up with its recent decisions on easing of Working Capital Financing, infusing liquidity in money markets, Greater access to MSF (Marginal Standing Facility), Permitting Banks to Deal in Offshore Non-Deliverable Rupee Derivative Markets (Offshore NDF Rupee Market) etc. Moreover, the RBI has already infused INR 280,000 crore, equivalent to 1.4% of Indian GDP, which along with the current tools announced by the RBI will result in liquidity injection of 3.2% of the GDP and is fully prepared to take ‘whatever tools are necessary—all instruments, conventional and unconventional are on the table’. Consequently, surplus liquidity in the banking system has increased sharply in the wake of sustained government spending.

Regional offices of the RBI have supplied fresh currency of INR1.2 lakh crore from March1 till April 14, 2020 to currency chests across the country to meet increased demand for currency in the recent scenario. RBI has even undertaken measures to target liquidity provision to sectors and entities which are experiencing liquidity constraints and/or hindrances to market access. It has been decided to conduct targeted long-term repo operations (TLTRO 2.0) for an aggregate amount of INR 50,000 crore, to begin with, in tranches of appropriate sizes. As confirmed by the RBI in the recent press release, the apex bank will review the operations and the situation and accordingly may increase the amount as per the requirement.

iv. Trade Balance:

Foreign direct investment (FDI) is one of the major sources of non-debt financial resource for the economic development of India. Foreign companies invest in India to take advantage of relatively lower wages, large consumer base, special investment privileges such as tax exemptions and for the benefit of ease of doing business.

According to the report shared by the Department for Promotion of Industry and Internal Trade (DPIIT), FDI equity inflows in India in April-December, 2019 stood at US$36.79 billion, indicating that government’s effort to improve ease of doing business and relaxation in FDI norms is giving positive results. As per the latest RBI Press Note, the trade deficit declined to US $9.8 billion in March 2020 from US $11 billion a year ago. After the economic activities resumes its operation post COVID-19, the Current Account deficit may be reduced by increasing the export on a large scale and decreasing the import of goods.

v. Growth in the Agricultural Sector:

The country’s agriculture sector accounts for 17% contribution in the GDP and has a growth rate of 3.4%. Approx. 55 cr population of the country is engaged in the agriculture sector which tantamount to 58% employment generation. Since agriculture sector is the prime sector employing the maximum population of India, so the Government focusses on increasing the percentage of the contribution to GDP from this sector. It has even been observed that by April 10, pre-monsoon kharif sowing had begun strongly, with acreage of paddy – the principal kharif crop – up by 37% in comparison with the last season. India has set up an ambitious goal of doubling farm income by 2022.

The farmers should now have a direct reach to the market so that they can sell their products in the market directly and at a reasonable rate; use of new techniques and technology to be introduced to attract youth to this sector and ultimately achieve better production and exports.

vi. Growth in GDP:

With the massive side effects of the pandemic spread, our dependence on the import of raw materials and consumer goods will be curtailed forcefully. Service industry will grow extensively, and tourism industry will be linked with the healthcare sector so as to give an added benefit to the youth employed. As per the RBI report, India is expected to post a sharp turnaround and resume its pre-COVID pre-slowdown trajectory by growing at 7.4 per cent in 2021-22. As the trade balance is maintained, Indian GDP is expected to make a remarkable growth in the next few quarters.

Steps already taken

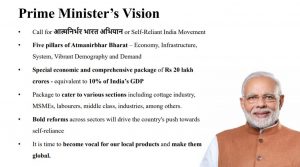

The Indian Government had recently announced economic package of INR1.7 lakh crores under Prime Minister Gareeb Kalyan Yojana to protect the poor citizens of the country from the economic impact of the nationwide lockdown and decided to defer the Tax and regulatory payments along with compliance filings as a relief to combat the existing crisis and for easy governance. The apex Bank has also come up with some positive arrangements to infuse liquidity in the market and control the turmoil. Some of the steps taken may be highlighted as below:

a) Money markets were facing pressures from redemptions by mutual funds. The Targeted Long-term Refinancing Operations (TLTRO) will ease the liquidity position of the banks, for which they were supposed to invest in investment-grade bonds, commercial paper etc. In order to reduce the adverse effects on the economic activity leading to pressures on cash flows, the RBI had decided to conduct auctions of targeted term repos of up to three years tenor of appropriate sizes for a total amount of up to ₹1,00,000 crore at a floating rate linked to the policy repo rate. This will reassure the money markets to work without the crunch of funds.

b) The RBI recently issued a press note confirming that they had a talk with the NABARD, SIDBI and NHB and accordingly decided to provide special refinance facilities for a total amount of INR 50,000 crore to NABARD, SIDBI and NHB to enable them to meet sectoral credit needs.

c) The cut of 75 basis points in repo rate is a powerful signal, aimed at lowering the cost of funds. The interest on floating rate housing loans will come down, helping household cash flows. Repo rate has come down to 4.40 % from 5.15%. The RBI also cuts the reverse repo rate two times, one by 90 basis points and another by 25 basis points, which has now come down to 3.75% to discourage banks to passively deposit funds with the RBI.

d) Liquidity coverage ratio requirement for Scheduled Commercial Banks has been brought down from 100% to 80% with effect from April 17, 2020.This requirement shall be gradually restored back in two phases – 90% by October 1, 2020 and 100% by April 1, 2021.

e) Health insurance scheme of INR 50 lakh for health workers fighting COVID-19 in Government Hospitals and Health Care Centres has been announced.

f) In order to help the poorest section of the society, a total of 20.40 crores PMJDY women account-holders would be given an ex-gratia of INR 500 per month till June, 2020 to help them run their household during this difficult period. The Government of India has also declared to spend INR 31,000 crores for this purpose.

g) Free gas cylinders, would be provided to 8 crore poor families till June, 2020 and three gas cylinders would be provided to the beneficiaries of Pradhan Mantri Ujjwala Yojana during this period.

h) Under National Rural Livelihood Mission Scheme, collateral free loans is doubled from INR 10 Lakhs to INR 20 lakhs to 63 lakhs Women Self Help Groups(SHGs) which would ultimately benefit 6.85 crore households.

i) It has been now decided that where the time limit of due dates for issue of notice, intimation, notification, approval order, sanction order, filing of appeal, furnishing of return, statements, applications, reports, any other documents and time limit for completion of proceedings by the authority and any compliance by the taxpayer, including investment in saving instruments or investments for roll over benefit of capital gains under Income Tax Act, Wealth Tax Act, Prohibition of Benami Property Transaction Act, Black Money Act, STT law, CTT law, Equalisation Levy law, Vivad Se Vishwas law is expiring between March 20, 2020 to June 29, 2020, it has been extended to June 30, 2020.

j) Taxpayers having aggregate annual turnover less than INR 5 crore will be allowed to file return under Form GSTR-3B due in March 2020, April 2020 and May 2020, till 30th June, 2020 without any interest, late fee, and penalty whereas others having annual turnover more than or equals to INR 5 crore will be allowed to file the same with a reduced interest of 9% p.a. instead of the existing 18% p.a., from 15 days after the relevant due date but without any late fee or penalty.

k) In order to reduce the burden and make the default good, the Ministry of Corporate Affairs has introduced Companies Fresh Start Scheme, 2020 and LLP Settlement Scheme, 2020 with a one-time relaxation to law abiding Companies and LLPs so as to enable them to complete their pending compliances without payment of any additional filing fees, thereby the entrepreneurs may focus on the growth of their businesses.

Recommendation:

An intensive study on the past economic performance of the Indian economy vis-à-vis the global economy and the effects of the COVID-19, a few recommendations are likely to be highlighted for the taking advantage of the better opportunities to the Indian economy:

a) The India Government should now focus on interacting with the business entities and Governments of various other countries to set up their manufacturing base in India. The Central and State Governments may set up specific workforce for interacting with the foreign investors and frame guidelines for timely completion of the projects. The said workforce may be formed jointly by the industry experts, professionals and Government representatives.

b) New guidelines for Foreign Portfolio Investment (FPI) may be introduced in order to safeguard the opportunistic takeovers/ acquisitions of the Indian businesses by way of indirect overseas investments.

c) While calculating the qualifying criteria of the non-performing assets (NPA) the lockdown period and the long-term economic impact of the COVID-19, may be excluded;

d) The Government may incentivize digitalization and facilitate payments through digital mode only and the charges on the credit card/ digital payments may also be waived off;

e) The compliance structure/norms may be diluted for the MSME sector in order to encourage ease of doing business in India. Post the COVID-19 effects, India is expected to have the largest job-market ready for youth population in the world by 2020-21 and this sector is sure to support India in improving its financial inclusion and mitigating the rural-urban divide. Several policy interventions along with technology and innovation will continue to play a pivotal role in creating a business- friendly atmosphere for the MSMEs;

f) There may be a reduction in the short-term GST rate for some specific sectors and further the GST deposit may be linked to the receipt of the amount for the services rendered to balance the cash flows for the time being. Presently GST deposit is based on the invoice raised and not on the payment basis. It can in return reduce the burden on the SME sector and in return reduce the defaults;

g) Tax compliances may be diluted and there may be a reduction in the Tax rate and interest rate on business borrowings in order to give relaxation to the manufacturers and the consumers. Tax rate reliefs may also be allowed to the proprietorship and partnership entities like the Companies;

h) In order to encourage export and reduce import, the Government may bring certain relaxations on the export compliances and also expedite the refund and duty drawback process to stabilize the cashflow operation;

i) There should be compulsory health and life insurance by the Government for the healthcare workers, police, Safai karamcharis who are working endlessly for eradicating this menace.

Conclusion

The recent reforms or policies taken up by the Government clearly demonstrates that the we are leaving no stone unturned to make India a better place to do business and to improve opportunities for all sections of society along with increasing prosperity. India now has the best opportunity to become the economic giant and work as ‘one-size-fits-all’ country and the best business destination in the world. India has always been a friendly partner to the other countries and has now even decided to relax the export of hydroxychloroquine to the USA on case to case basis. It is good to quote that in the coming days India will be the prime source for supply of all essential and life saving commodities to the world. The World Trade Organisation sees global merchandise trade contracting by as much as 13-32 per cent in 2020. Activity in the corporate bond market has picked up appreciably, with several corporates making new issuances. The level of foreign exchange reserves continue to be robust at US $ 476.5 billion on April 10, 2020 equivalent to 11.8 months of imports. India is expected to become the next economic powerhouse with its core competencies.

In order to put a further check on the import of goods, the Government may increase the duty on import of consumer goods and incentive to be given to the MSME sector in order to encourage the production of goods and increase the exports of the country. New technologies are required to be used in the cottage and rural divisions. The government incentives are required to be increased in the manufacturing sector along with easy accessibility of finance and market to the youth so that they can engage themselves in this sector and can start manufacturing without any marketing or financial difficulty.

Written & Compiled by CA Sunil Kumar Gupta

Founder Chairman, SARC Associates

www.sarcassociates.com