In a momentous stride towards global collaboration and dialogue, Mr. Vijay Goel and Mr. Sunil Kumar Gupta, Founders of Indo European Business has visited Switzerland to represent IEBF at the esteemed World Economic Forum (WEF) Annual Meeting Davos, slated to transpire against the breathtaking backdrop from January 15th to January 19th, 2024.

Justify Text Alignment

IEBF has achieved a significant milestone during its visit to the WEF Annual Meeting, marked by the successful signing of Memoranda of Understanding (MoUs) with the Government of Karnataka in the prescence of Dr. Ekroop Caur, IAS, Secretary to Government, Department of Electronics, Information Technology, Biotechnology and Science & Technology; Sh. LK Atheeq, IAS, Additional Chief Secretary to Chief Minister Government of Karnataka; Smt. Gunjan Krishna, IAS, Commissioner for Industrial Development & Director of Industries & Commerce CEO, Invest Karnataka Forum, among other dignitaries. These agreements symbolize a shared commitment to pioneering initiatives that are poised to make a lasting impact on various sectors. Here are the key collaborations:

1. Manufacturing of Solar Panels, Inverters, and EV Charging Plants with Ampergia Americans:

– Contributing to clean energy solutions and sustainable technology, boosting Karnataka’s leadership in renewable energy.

2. Providing Services for Employee Welfare Programmes with InstaPe Synergies Pvt. Ltd.:

– Providing services that enhance the well-being of our workforce, fostering a supportive and motivated work environment.

3. Construction of Biopharmaceuticals and Cancer Diagnosis and Treatment Hospitals with Pangaea Data:

– Spearheading healthcare infrastructure development, aiming to improve accessibility and outcomes in Karnataka.

4. Manufacture of “Smart City” Infrastructure with Faction AI:

– Enhancing urban living through innovative infrastructure solutions, contributing to the development of Smart Cities.

These collaborations underscore IEBF’s commitment to fostering positive change. Additionally, IEBF is in the process of signing various MoUs with distinct State Government, further expanding India’s impact in global market.

Adding to the grandeur of this international gathering, the WEF witnessed the participation of five prominent Indian states – Maharashtra, Karnataka, Uttar Pradesh, Telangana, and Tamil Nadu. This collective representation is designed to showcase the diverse tapestry of Indian culture, economic prowess, and historic richness, symbolizing the nation’s multifaceted essence on the global landscape.

“This opportunity not only underscores the cultural, economic, and historic opulence of India but also reinforces our commitment to global collaboration and the pursuit of a more interconnected world,” Mr. Gupta stated.

This visit comes as a recognition of Mr. Goel and Mr. Gupta’s exceptional contributions and leadership in the growth of India, EU, UK, and Slovenia. Eagerly anticipating the opportunity to engage in profound discussions and collaborative endeavors, Mr. Gupta is poised to lend their perspective towards charting a course for a more promising future on the global stage.

Under the visionary leadership of Mr. Sunil Kumar Gupta, the Indo European Business Forum (IEBF) has recently spearheaded a groundbreaking Indo-Slovenian partnership. Since its inception in 2017, IEBF has played a pivotal role in facilitating the success of approximately 85% of businesses, ushering in excellence across diverse sectors such as business, finance, real estate, and art.

IEBF’s impactful initiatives extend to aiding 80% of businesses and investors in identifying lucrative investment opportunities within EU countries, the UK, and India. Mr. Goel and Mr. Gupta’s strategic leadership has positioned IEBF as a key player in fostering international collaborations, contributing significantly to the growth and success of businesses on a global scale. The forum’s commitment to excellence and its role in connecting diverse industries underscore their dedication to advancing economic partnerships and creating a robust global business network.

The Founders of IEBF, Mr. Vijay Goel and Mr. Sunil Kumar Gupta had the honor of meeting with the Hon’ble Chief Minister of Maharashtra and the Hon’ble Minister for Large & Medium Industries and signing various MoUs. These engagements highlight our dedication to strong partnerships and collaborations, reinforcing IEBF’s role in shaping a sustainable and connected future.

The World Economic Forum serves as a splendid platform for thought leaders, influencers, and decision-makers to converge and discuss critical global issues. The participation of world leaders, businessmen, professionals and the delegation from five prominent Indian states adds a unique perspective to the ongoing dialogue.

The introduction of four New Labour Codes introduced by the Government of India represents a significant step towards reforming and strengthening labour laws in India. The Code on Wages was enacted by the Parliament in August 2019, followed by the Industrial Relations Code in September 2020. Similarly, the Code on Social Security and the Occupational Safety, Health, and Working Conditions Code were also enacted by the Parliament in September 2020. These legislative actions signify a comprehensive effort to reform and streamline labor laws, addressing various aspects related to wages, industrial relations, social security, and occupational safety and health. The synchronized enactment of these codes demonstrates a holistic approach toward creating a more coherent and contemporary framework for labor regulations in the country.

Justify Text Alignment

The landmark decision to consolidate 29 laws into four codes is a historic step toward providing women with not only job security but also respect, health, and various welfare measures. Through these labor reforms, there is a clear commitment to creating an environment that prioritizes the well-being of women in the workforce. Additionally, these changes are expected to significantly enhance the ease of doing business in the country, streamlining regulations and fostering a more conducive environment for both employers and employees. This forward-looking approach not only supports gender equality but also contributes to the overall economic development and business efficiency in the nation.

In this comprehensive reform, the government seeks to ensure that all workers have a statutory right to receive minimum wages and timely wage payments, fostering a more equitable and prosperous labour environment. To reduce ambiguity and legal disputes, these codes introduce uniform and straightforward definitions of ‘wages’ across all four labour-related regulations. Furthermore, the introduction of annual health check-ups and medical facilities aims to improve the overall well-being of workers, enhancing productivity and extending life expectancy.

These reforms also formalize the employment relationship by requiring the issuance of appointment letters to every employee, ultimately providing job security and enabling workers to claim statutory benefits such as minimum wages and social security. Additionally, the creation of a Re-skilling Fund demonstrates the government’s commitment to the skill development of workers, aligning with the changing demands of the job market.

Furthermore, the codes recognize the importance of addressing the needs of gig workers and platform workers by defining them and paving the way for the formulation of social security schemes funded by aggregators and government sources. This inclusive approach extends the benefits of the Employees’ State Insurance Corporation and the Employees’ Provident Fund Organization to unorganized workers, gig workers, and platform workers, along with their families.

The reforms also ensure that fixed-term employment (FTE) workers are entitled to the same benefits as permanent employees, promoting fairness and job security. Workers’ rights are further enhanced with provisions for annual leave with wages and the option to encash leave on demand, offering flexibility and financial security.

Moreover, the expansion of the Employees’ Provident Fund to all industries, irrespective of their scheduling, underscores the government’s commitment to improving social security and labour welfare across various sectors. In sum, these labour codes represent a transformative and forward-looking effort to foster a more inclusive, secure, and prosperous work environment for all workers in India.

The four Labour Codes aim to enhance worker protection, including those in the unorganized sector, by ensuring statutory minimum wages, social security, and healthcare. Some significant provisions of these Codes include:

Establishing a statutory right for all workers to receive minimum wages and timely wage payments to support sustainable development and inclusivity.

Introducing a consistent and easily enforceable definition of ‘wages’ across all four Labour Codes to prevent multiple interpretations and legal disputes.

Providing annual health check-ups and medical facilities to enhance worker productivity and increase life expectancy.

Requiring the issuance of appointment letters to every employee, formalizing employment contracts, increasing job security, and enabling workers to claim statutory benefits such as minimum wages and social security.

Establishing a Re-skilling Fund for worker skill development.

Defining gig workers and platform workers to create social security schemes, funded by aggregators and other sources, with contributions from both the Central and State Governments.

Allowing the Central Government to extend benefits to unorganized workers, gig workers, platform workers, and their families through the Employees’ State Insurance Corporation and the Employees’ Provident Fund Organization.

Granting fixed-term employment (FTE) workers entitlement to the same benefits available to permanent employees, including gratuity after one year of service.

Ensuring that every worker is entitled to annual leave with wages after working for 180 days, compared to the current requirement of 240 days. Additionally, there is a provision for leave encashment on the worker’s request while in service at the end of the calendar year.

Expanding the applicability of the Employees’ Provident Fund to all industries, as opposed to only scheduled industries as it stands presently.

Major Achievements of New Labour Codes are as follows –

As of December 2023, the Shram Suvidha Portal has successfully generated 4,268,334 Labour Identification Numbers (LIN). Furthermore, inspection reports for 821,283 cases have been uploaded onto the portal, reflecting the ongoing efforts to monitor and manage labor-related activities.

The eSHRAM portal has been established with the aim of building a National Database of Unorganized Workers, incorporating Aadhaar details to facilitate the provision of social security benefits. Eligibility for registration on the eSHRAM portal is open to any worker operating in the unorganized sector with an age ranging from 16 to 59. This database encompasses a diverse range of workers, including migrant workers, construction workers, gig workers, platform workers, and more. As of December 2023, a noteworthy achievement has been reached, with a total of 29,23,93,908 e-cards issued through the portal, marking a significant step in the coverage and support for unorganized workers across the nation.

As of October 2023, the All India Consumer Price Index Number for Industrial Workers (CPI-IW) has experienced a rise of 0.9 points, reaching a value of 138.4 (one hundred thirty-eight point four). In terms of the one-month percentage change, there has been a 0.65% increase compared to the previous month. This is in contrast to the 0.91% increase recorded during the corresponding months of the previous year. These figures provide insights into the fluctuations in the cost of living and inflationary trends affecting industrial workers in India.

As part of the Nidhi Aapke Nikat 2.0 initiative, the Employees’ Provident Fund Organization (EPFO) extended its outreach to stakeholders across all districts of the country. The monthly ‘Nidhi Aapke Nikat’ program held on April 27th, 2023, covered 666 districts with 27,592 participants. The focus was on addressing grievances, resulting in 12,437 reported issues, of which 9,816 were successfully resolved. This effort underscores EPFO’s commitment to increasing accessibility, visibility, and resolving concerns for its stakeholders nationwide.

As part of the celebration of Azadi Ka Amrit Mahotsav (AKAM), the Employees’ Provident Fund Organization (EPFO) has initiated a special drive to promote the filing of e-nominations by its members. In the month of September 2023, a notable achievement was reached with the filing of 3.40 lakh e-nominations. Cumulatively, as of September 30, 2023, a total of 2.07 crore e-nominations have been successfully filed, reflecting the widespread participation of members in utilizing the digital nomination process facilitated by EPFO. This effort aligns with the organization’s commitment to modernize processes and enhance member convenience.

The provisional payroll data released by EPFO in November 2023 reveals a positive trend, indicating the addition of 891,583 net subscribers during the month of September 2023. This data underscores the ongoing growth and engagement within the Employees’ Provident Fund Organization, with a substantial number of individuals being added to the workforce during the specified period.

As part of the ‘Prayaas’ initiative, the field offices of EPFO have been actively distributing Pension Payment Orders (PPOs) to members of the Employees’ Pension Scheme 1995 on the day of their superannuation. Until September 30, 2023, the field offices conducted a total of 6,751 webinars to promote and educate stakeholders about the Prayaas initiative. Furthermore, during the month of September 2023 alone, 403 PPOs were successfully handed over to subscribers, highlighting the commitment of EPFO to streamline processes and enhance member services through proactive initiatives like Prayaas.

As part of the efforts to boost employment generation and mitigate the socio-economic impact of the Covid-19 pandemic, the Ministry of Labour & Employment introduced the EPFO-linked Aatmanirbhar Bharat Rojgar Yojana (ABRY) scheme on December 30, 2020. As of September 23, 2023, a total of 1,52,452 establishments have likely participated in the scheme, contributing to the broader objective of fostering economic recovery and job creation in the wake of the pandemic.

While the government has undertaken several initiatives to promote employment generation in both the organized and unorganized sectors of the economy, we emphasize the need for a substantial focus on physical outreach and alternative methods. This consideration arises from the fact that a significant portion of the labor force in India lacks access to the internet or smartphones. To ensure the inclusivity of employment-related initiatives, there is a necessity to incorporate strategies that reach individuals who may face barriers to online engagement, thereby ensuring a more comprehensive and effective approach to address the diverse needs of the labor workforce.

In this article, we will delve into some of the vital provisions and implications of these groundbreaking New Labour Codes, shedding light on their potential to improve the lives of countless workers across India.

4 New Labour Codes – a revolutionary approach to protecting the interests of workers

Labour laws in India had their origins in the British Raj, but over time, many of these laws had become obsolete and ineffective. Instead of safeguarding workers’ interests, some of these outdated labour codes had hindered their progress.

In response to this, the then-current government recognized the need to eliminate redundant or irrelevant labour laws. Consequently, the 29 existing labour laws were streamlined and consolidated into 4 new labour codes, a move that was expected to bring significant benefits to all stakeholders.

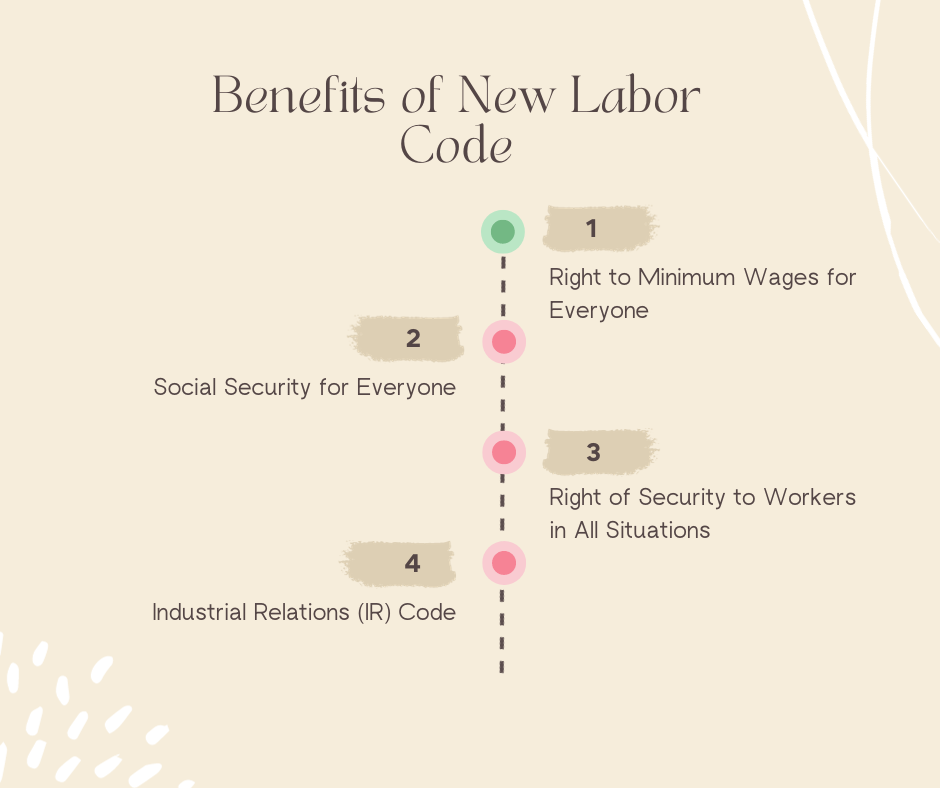

Benefits of New Labour Code

Right to Minimum Wages for Everyone

4 labour laws are amalgamated into the Minimum Wage Code which has provided the “right to minimum wages” for the first time.

Labour Code (Wage Code) – 2019

For the first time since India’s independence, the government is actively working towards providing wage security, social security, and health security to workers in both organized and unorganized sectors.

The assurance of minimum wages extends to workers in both organized and unorganized sectors.

Review of minimum wage rates every five years.

Workers will get timely payment of their wages as a guaranteed right.

Male and female workers will receive equal remuneration for their work.

Approximately 400 million unorganized workers now have the right to a minimum wage, a significant development.

The introduction of a floor wage aims to eliminate regional disparities in minimum wage levels.

Determining minimum wages has been simplified by basing it on criteria like skill level and geographical locUnder National Data Governance Policy, GoI to set up 1 hundred labs in order to develop applications using 5G services in engineering institutions to realize a new range of opportunities, business models, and employment potential.

Increased wage ceiling from Rs 18,000 to Rs 24,000 in FY 28-08-2017.

In the recent G20 Summit, providing quality employment was one of the commitments. India is committed to promoting sustainable, quality, healthy, safe, and gainful employment. This commitment emphasizes the importance of employment that not only provides income but also contributes to overall well-being and safety.

In order to guarantee security for all workers, the Central Government consolidated nine Labour Laws into the Social Security Code. This step was taken to safeguard workers’ rights to insurance, pensions, gratuity, maternity benefits, and more.

Through this Code, a comprehensive legal framework for Social Security was established, ensuring that workers could fully access social security benefits.

Under this initiative, a systematic approach was put in place for contributions from both employers and workers. Additionally, the government had the capacity to subsidize contributions from workers in disadvantaged sections.

Social Security Code, 2020

By making a nominal contribution, individuals can access the privilege of receiving free medical treatment at ESIC hospitals and dispensaries.

The accessibility of ESIC will now be extended to workers across all sectors, including those in the unorganized sector.

The expansion of ESIC hospitals, dispensaries, and branches will now reach the district level, extending this service from the existing 566 districts to cover all 740 districts in the country.

ESIC benefits are extended to any worker involved in hazardous work, even if it’s just a single worker.

Platform and gig workers in emerging technology fields have the opportunity to join ESIC.

Plantation workers to get benefit of ESIC.

Institutions operating in hazardous areas are required to undergo mandatory registration with ESIC.

Expansion of Social Security

The pension scheme (EPFO) benefits will be extended to workers in both organized and unorganized sectors, including those who are self-employed.

A social security fund is being established to deliver all-encompassing social security support to the unorganized sector.

The necessity for a minimum service requirement to receive gratuity has been eliminated for fixed-term employees.

Fixed-term employees are entitled to receive the same social security benefits as permanent employees.

The establishment of a national worker database for the unorganized sector will be achieved through registration on a dedicated portal.

Employers with a workforce of over 20 employees are required to submit job vacancies online.

A Universal Account Number (UAN) will be introduced to cover ESIC, EPFO, and workers in the unorganized sector.

A Universal Account Number (UAN) based on Aadhaar to ensure effortless portability.

Right of Security to Workers in All Situations

To enhance workplace safety and occupational health for workers, the Occupational Safety, Health, and Working Conditions Code, 2020 has consolidated 13 existing labour laws. This Code prioritizes safeguarding the interests of workers in various sectors, including factories, mines, plantations, the motor transport industry, bidi and cigar workers, as well as contract and migrant workers.

OSH Code (Occupational, Safety, Health, Working Condition) – 2020

Numerous provisions within the OSH Code will improve the living conditions and well-being of Inter-State Migrant Workers.

The OSH Code has effectively resolved the discrepancies present in the Inter-State Migrant Workers Act, 1979. In the past, only workers hired by a contractor were acknowledged as Inter-State Migrant Workers. However, the updated provisions in the Code empower workers to become self-reliant by allowing them to self-register as Inter-State Migrant Workers on the national portal. This registration grants them a legal identity, enabling access to the benefits of various social security schemes.

An arrangement has been put in place for employers to offer an annual travel allowance to Inter-State Migrant Workers for their round-trip journey to their hometown.

Mandatory issuance of appointment letters to workers has been implemented.

Employers are required to provide workers with a mandatory and cost-free annual health check-up.

Workers engaged in construction and related activities, working in one state and relocating to another state, will receive benefits from the Building and other Construction Workers’ Cess fund.

The “One Nation – One Ration Card” initiative ensures that an Inter-State Migrant Worker can access ration benefits in the state where they are employed, while the rest of their family can avail these benefits in the state where they reside.

A national database will be established for Inter-State Migrant Workers.

Now, if a worker has worked for 180 days, they will be entitled to one day of leave for every 20 days of work completed, instead of the previous requirement of 240 days.

Women Empowerment Through New Labour Codes in India

Women workers have the right to work in all categories of establishments.

Women now possess the right to work during nighttime with their consent, and employers must ensure adequate safety and facilities for women workers during night shifts.

In 2017, amendments were made to the Maternity Benefit Act to extend paid maternity leave for female workers from 12 weeks to 26 weeks and mandate the availability of crèche facilities in all establishments employing 50 or more workers.

Industrial Relations (IR) Code

Through the amalgamation of three Labour Laws into the Industrial Relations Code, the Central Government has taken measures to protect the interests of both Trade Unions and workers. This Code encompasses various provisions aimed at ensuring the harmony and minimizing potential disputes between industrial units and workers in the future.

Towards the end of disputes (Industrial Relations Code) –

In the event of job loss, workers will be eligible for benefits under the Atal Bimit Vyakti Kalyan Yojna.

The Atal Bimit Vyakti Kalyan Yojna offers financial assistance to organized sector workers who lose their jobs, serving as a form of unemployment allowance. This benefit is available to workers enrolled in the ESI Scheme.

During the retrenchment process, workers will receive 15 days’ worth of wages dedicated to re-skilling. These wages will be directly deposited into the worker’s bank account, facilitating their ability to acquire new skills.

Accelerated delivery of justice to workers via the Tribunal.

Resolution of workers’ disputes in the Tribunal within one year.

Industrial Tribunals will consist of two members to expedite the resolution of cases.

In industrial establishments, a Trade Union that secures 51 percent of the votes will be acknowledged as the exclusive negotiating union with the authority to engage in agreements with employers.

In industrial establishments where no trade union garners 51 percent of the votes, a negotiating council of trade unions will be formed to facilitate agreements with the employer.

Welfare of Inter-State Migrant Workers

The government has devoted considerable effort to enhance the welfare of Inter-State Migrant Workers. Measures have been implemented to fortify the legal framework concerning these workers.

For the benefit of Inter-State Migrant Workers and those in need, the Central Government has expedited various schemes, such as Garib Kalyan and the delivery of free food grains to households.

Benefits of Codification

Single Registration; Single License; Single Statement; Minimum Forms

Common definitions

Reduction of Committees

Web-based surprise inspection

Use of technology – Electronic registration and licensing

Reduction of compliance cost and disputes

Impact of New Labour code

The impact of the new Labour Codes in India is multifaceted and has several implications for the labour landscape, the economy, and society as a whole:

Enhanced Worker Protection: The introduction of statutory rights to minimum wages and timely wage payments provides workers with financial security, reducing the risk of exploitation and poverty among the labour force. This can lead to improved living standards for a significant portion of the population.

Formalization of Employment: Requiring employers to issue appointment letters formalizes employment relationships, increasing job security and ensuring that workers can claim their rightful benefits. This formalization can lead to more stable employment conditions for workers.

Skill Development: The creation of a Re-skilling Fund emphasizes the importance of keeping the workforce up to date with evolving job market demands. This can lead to a more skilled and adaptable labour force, contributing to economic growth.

Inclusion of Gig Workers: Recognizing and providing social security benefits to gig and platform workers acknowledges the changing nature of work. This can improve the working conditions and welfare of a significant segment of the workforce.

Equal Treatment for Fixed-Term Employees: Ensuring that fixed-term employees receive the same benefits as permanent employees promotes fairness in employment practices and job security for a wider range of workers.

Improved Health and Well-being: The provision for annual health check-ups and medical facilities enhances workers’ overall health and productivity. Healthier workers tend to be more efficient and have a longer work life, contributing to economic growth.

Streamlined Definitions and Regulations: The introduction of uniform definitions of ‘wages’ simplifies compliance for employers and reduces legal disputes. This can lead to more efficient labour market operations and less administrative burden for businesses.

Social Security Expansion: Extending social security benefits to unorganized workers, gig workers, platform workers, and their families provides a safety net for a larger portion of the workforce. This can reduce economic vulnerabilities and improve social welfare.

Promotion of Gender Equality: Provisions promoting gender equality can empower women to participate more actively in the labour force, potentially leading to increased economic output and improved social inclusivity.

Economic Growth and Productivity: Overall, the Labour Codes can contribute to economic growth by ensuring a more efficient and inclusive labour market. With a protected and skilled workforce, businesses can operate more effectively, leading to increased productivity and, in turn, economic growth.

Reduced Administrative Burden: Simplifying regulations and compliance can reduce the administrative burden on businesses, making it easier for them to focus on growth and expansion.

Legal Clarity: The Labour Codes bring about legal clarity with standardized definitions and regulations. This can reduce legal disputes and lead to a more predictable and stable labour environment.

Improved Working Conditions: The codes have provisions for better working conditions and safety, ensuring that workers are healthier and more motivated, which can lead to improved productivity.

The introduction of the Labour Codes in India represents a significant step toward reforming labour laws and has far-reaching implications for workers, employers, and the broader economy. The impact is expected to be positive, promoting better labour conditions, inclusivity, and economic growth. However, the successful implementation and enforcement of these codes will be critical to realizing these potential benefits fully.

Conclusion

In conclusion, the introduction of the four Labour Codes in India represents a transformative step towards reforming and strengthening labour laws in the country. These codes, which include the Code on Wages, 2019, the Industrial Relations Code, 2020, the Code on Social Security, 2020, and the Occupational Safety, Health, and Working Conditions Code, 2020, are not only significant in their scale but also in their potential to create a more equitable, secure, and prosperous work environment for all.

These codes address various aspects of labour rights and welfare, with a primary goal of safeguarding the interests of workers, especially those in the unorganized sector. Some of the notable provisions include the establishment of a statutory right to minimum wages and timely wage payments, simplified definitions of ‘wages’ to reduce ambiguity, annual health check-ups and medical facilities to enhance worker well-being, and the mandatory issuance of appointment letters to formalize employment relationships.

Additionally, these codes recognize the changing nature of work and the emergence of gig workers and platform workers in new technology sectors. They lay the groundwork for social security schemes for these workers, funded through contributions from aggregators and government sources. This inclusivity extends the benefits of social security to unorganized workers, gig workers, and platform workers, along with their families.

Moreover, the codes promote fairness and job security by ensuring that fixed-term employment (FTE) workers are entitled to the same benefits as permanent employees. Workers are also granted enhanced rights, such as annual leave with wages and the option to encash leave. The extension of the Employees’ Provident Fund to all industries, irrespective of their scheduling, further underscores the government’s commitment to improving social security and labour welfare.

These labour codes are not just an exercise in legal reform; they signify a comprehensive shift towards better protection, security, and welfare for all workers in India. They aim to reduce disputes, ensure faster resolution of labour issues, and provide social security for workers across various sectors and backgrounds. By streamlining and consolidating labour laws, they reduce the compliance burden and contribute to economic and social development.

Furthermore, the specific focus on Inter-State Migrant Workers and women workers adds an essential dimension to these reforms. Provisions for Inter-State Migrant Workers enable them to gain legal identity and social security benefits, while women workers are granted rights to work at night with safety measures in place. The extension of maternity leave and mandatory crèche facilities underlines the commitment to women’s empowerment.

In essence, the four Labour Codes represent a holistic and forward-looking approach to labour reform. They aim to protect the interests of workers, reduce disputes, and promote social security and well-being. As India continues to evolve and diversify its labour force, these codes offer a promising foundation for a more inclusive, equitable, and secure work environment for all its workers. They signify a significant stride towards progress and prosperity in the labour sector, aligning with the nation’s aspirations for sustainable growth and inclusivity.

Introduction & Need for RBI Central Bank Digital Currency

A total of 114 nations, India included, are actively considering digital currency adoption, with India already introducing its retail Central Bank Digital Currency (CBDC) on a pilot basis. The Reserve Bank of India envisions the e-Rupee, overseen and issued by the central bank, as the next-generation, seamless, widely accessible, and anonymous payment method designed to provide enhanced value to customers.

Justify Text Alignment

In FY 2023 (October 2023), India has registered 11,408.79 million transactions.

The evolution of technology aligns with the evolving needs of end-users, leading to an increasing number of payment use cases. Payments are integral to any financial institution, prompting central banks to explore avenues that offer innovative functionalities. Central Bank Digital Currency (CBDC) stands out as one such avenue, envisioned by the Reserve Bank of India (RBI) as the next-generation, seamless, ubiquitous, and anonymous payment mode, providing customers with enhanced value and a seamless experience.

The introduction of e-Rupee, the digital form of fiat currency regulated by the RBI, offers a viable alternative to paper currency. As the circulation of physical currency increases, it poses challenges to distribution and storage channels and has environmental implications, contributing to a carbon footprint. Moreover, increased cash circulation raises risks such as counterfeiting, spoilage, security threats, and the potential for loss or theft.

The launch of e-Rupee not only addresses these challenges but also aligns with the shift towards a digital economy. With the growing adoption of mobile and internet-based payments in India, CBDC can streamline cross-border transactions, a priority in the G20 summit. CBDC can mitigate the complexities associated with time-consuming processes and strict compliance checks in cross-border transactions, providing a more efficient and automated method for transaction and settlement. Additionally, CBDC has the potential to enhance various areas, including government securities and international forex trade.

The design of CBDC plays a crucial role, and its implications for payment systems, monetary policy, and the overall financial system depend on its intended functions. The RBI’s concept note emphasizes the importance of careful consideration in designing CBDC to ensure its positive impact on the financial landscape.

What is Digital Rupee | What is Central Bank Digital Currency CBDC

India has made significant strides in innovation in digital payments, supported by a separate law for Payment and Settlement Systems. The country now boasts state-of-the-art payment systems that are affordable, accessible, convenient, efficient, secure, and available round the clock. This transformation in payment preferences is largely due to the establishment of electronic payment systems like Real Time Gross Settlement (RTGS), National Electronic Funds Transfer (NEFT), Immediate Payment Service (IMPS), Unified Payments Interface (UPI), and mobile-based systems like Bharat Bill Payment System (BBPS) and National Electronic Toll Collection (NETC).

These developments have shifted the payments ecosystem, reducing reliance on cash and paper. The involvement of non-bank FinTech firms as Payment Instrument Issuers (PPIs), Bharat Bill Payment Operating Units (BBPOUs), and third-party application providers in the UPI platform has further accelerated the adoption of digital payments, with the Reserve Bank playing a catalytic role in promoting a safe, secure, and efficient payment system.

According to the 2018 report from CPMI-MC, there is a unique form of central bank money known as digital rupee/ money that is different from physical cash or central bank reserve or settlement accounts. This form of money has four distinct properties –

Issuer; whether it is a central bank or not

Form; whether it is in digital form or physical form

Accessibility; whether it is wide or narrow

Technology; whether it is peer-to-peer tokens or accounts

The digital rupee, or Central Bank Digital Currency (CBDC), represents a digitally native form of sovereign currency that replicates all the characteristics of physical currency. The RBI’s CBDC is strategically designed to instill structure and stability into the financial system through its multifaceted functions.

According to the Reserve Bank of India (RBI), a Central Bank Digital Currency (CBDC) is a digital manifestation of legal tender issued by the central bank. This currency holds a sovereign status and can be exchanged on a one-to-one basis with fiat currency.

Central Bank Digital Currency (CBDC) has emerged as a prominent subject of discussion in India, particularly in light of the potential introduction of the digital rupee by the Reserve Bank of India (RBI). Keyhighligts of the Digital Rupee are as follows:

The Central Bank digital currency RBI is a sovereign currency issued by the Central Bank in accordance with monetary policy.

CBDC represents a liability for the Central Bank.

It is expected that Central Bank Digital Currency (CBDC) should be widely accepted as a medium of payment, legal tender, and a secure store of value by all citizens, businesses, and government entities.

The aim is to reduce the cost of issuing money and conducting transactions.

It is a convertible legal tender, allowing individuals (holders) to use it without the necessity of a bank account.

CBDC can be voluntarily converted into commercial bank money and cash.

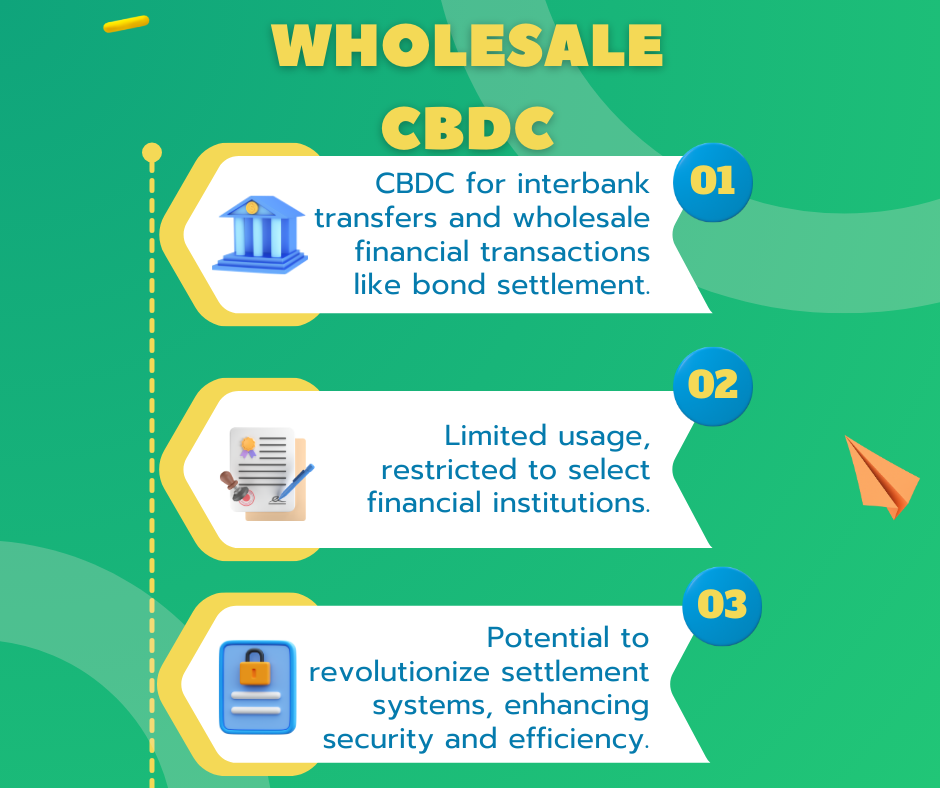

Types of CBDC or e-Rupee issued: Retail and wholesale

Source: www.rbi.org.in

Role of Central Bank and Other Entities: Who administers the CBDC

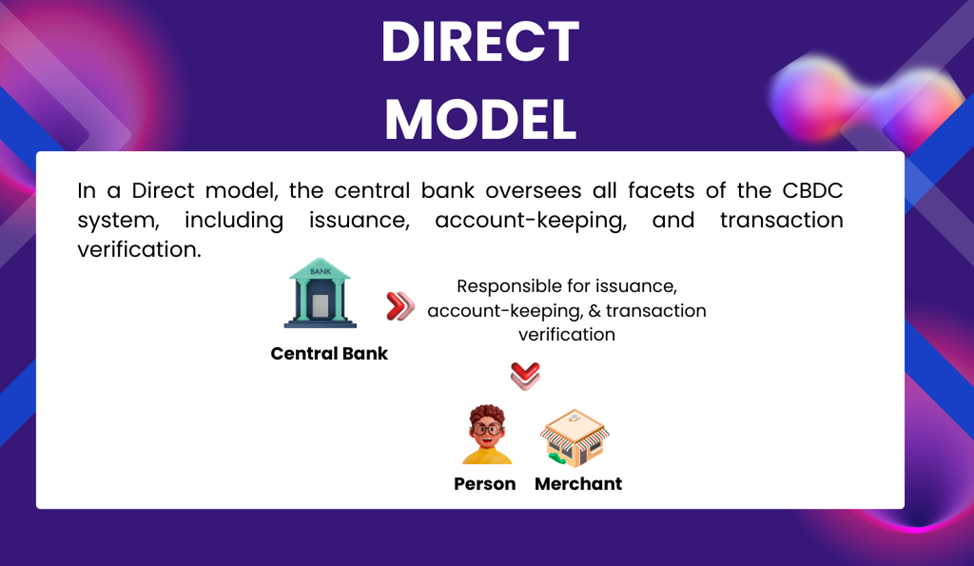

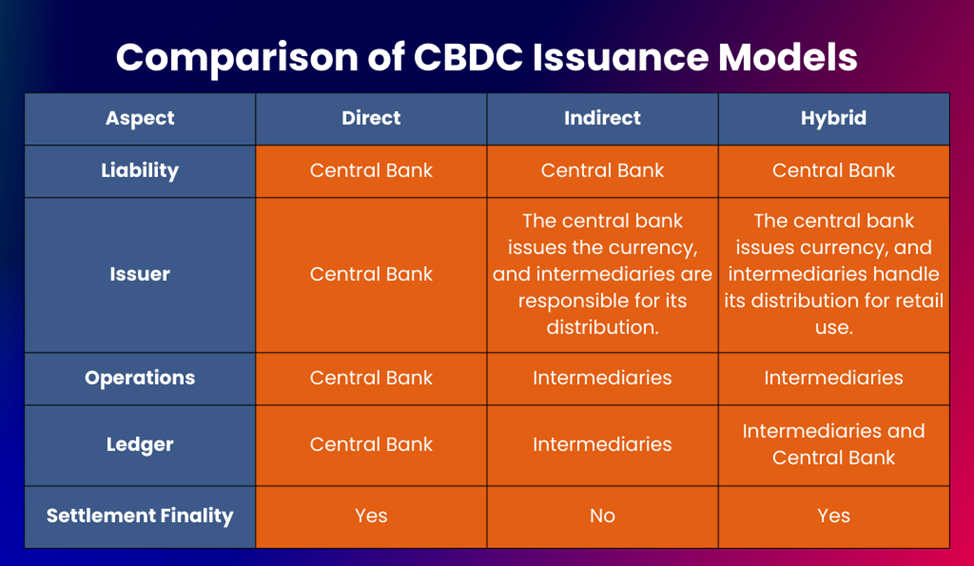

1. Single Tier Model (Direct CBDC Model):

The described model is referred to as the “Direct CBDC Model”. In this system, the central bank assumes responsibility for overseeing all aspects of the CBDC system, including issuance, account-keeping, and transaction verification. Under this model, the central bank manages the retail ledger, and its server is integral to all payment processes. The CBDC in this setup serves as a direct claim on the central bank, maintaining a comprehensive record of all balances and updating it with each transaction. This design ensures a highly resilient system, as the central bank possesses complete knowledge of retail account balances, facilitating straightforward verification and claim honoring.

However, a notable drawback of this model is its tendency to sideline private sector involvement, impeding innovation within the payment system. It is crafted for disintermediation, where the central bank directly engages with end customers. While offering disruptive potential for the current financial system, this model places an additional burden on central banks. The challenges include the direct management of customer onboarding, Know Your Customer (KYC) procedures, and Anti-Money Laundering (AML) checks, which could prove challenging and costly for the central bank.

Source: www.rbi.org.in

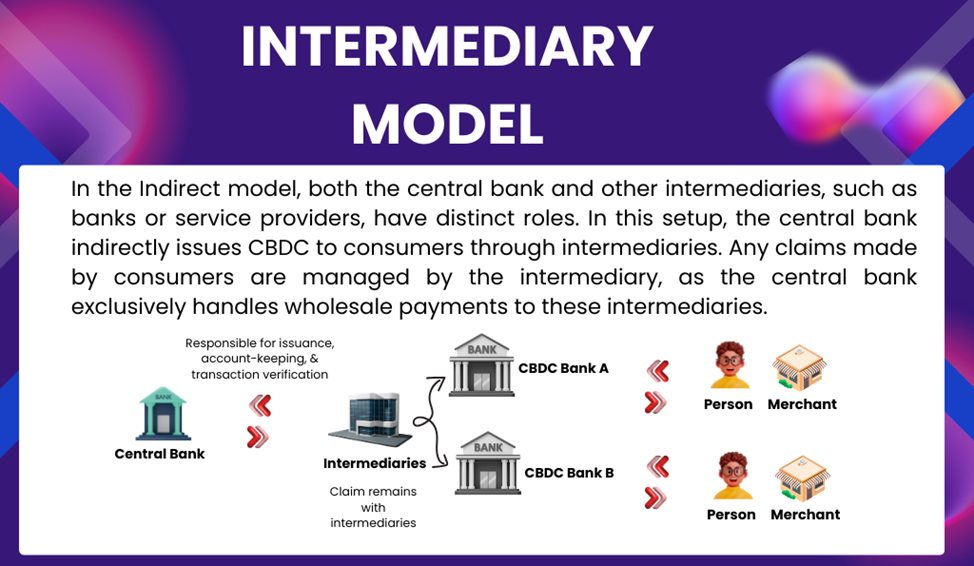

2. Two Tier Model (Intermediate model):

The inefficiency linked to the Single-tier model necessitates the design of CBDCs within a two-tier system, where both the central bank and other service providers have distinct roles. Within the intermediate architecture, there are two models: the Indirect Model and the Hybrid Model.

In the Indirect Model, consumers would maintain their CBDC in an account or wallet with a bank or service provider. The responsibility to provide CBDC upon demand rests with the intermediary rather than the central bank. The central bank’s role is limited to tracking the wholesale CBDC balances held by intermediaries, ensuring alignment with the total retail balances held by individual customers.

Source: www.rbi.org.in

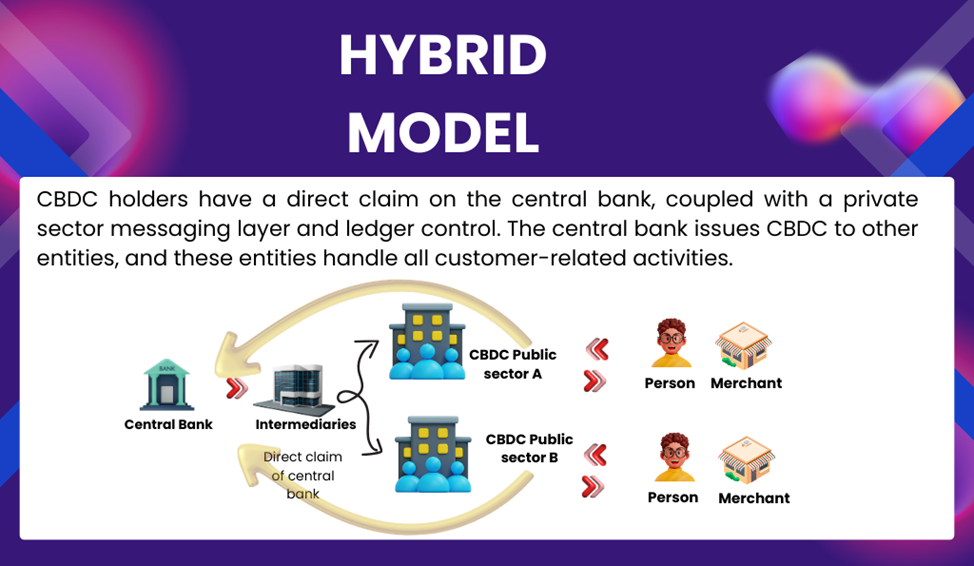

In the Hybrid model, a direct claim on the central bank is merged with a private sector messaging layer. In this arrangement, the central bank issues CBDC to other entities, making these entities responsible for all customer-associated activities. Commercial intermediaries, such as payment service providers, deliver retail services to end-users, while the central bank maintains a ledger of retail transactions.

Source: www.rbi.org.in

Comparison of CBDC Issuance Models

Form of design: Token based and account based

Central Bank Digital Currencies (CBDCs), being electronic representations of sovereign currency, should encompass all the essential features of physical currency. The design of CBDCs depends on the functions they are intended to fulfill, and this design has significant implications for payment systems, monetary policy, and the structure and stability of the financial system. It is crucial that the design features of CBDCs are minimally disruptive.

Key design choices when considering the issuance of CBDCs include:

Type of CBDC: Determining whether it will be a Wholesale CBDC, a Retail CBDC, or a combination of both.

Models for Issuance and Management: Choosing between a Direct model, an Indirect model, or a Hybrid model for issuing and overseeing CBDCs.

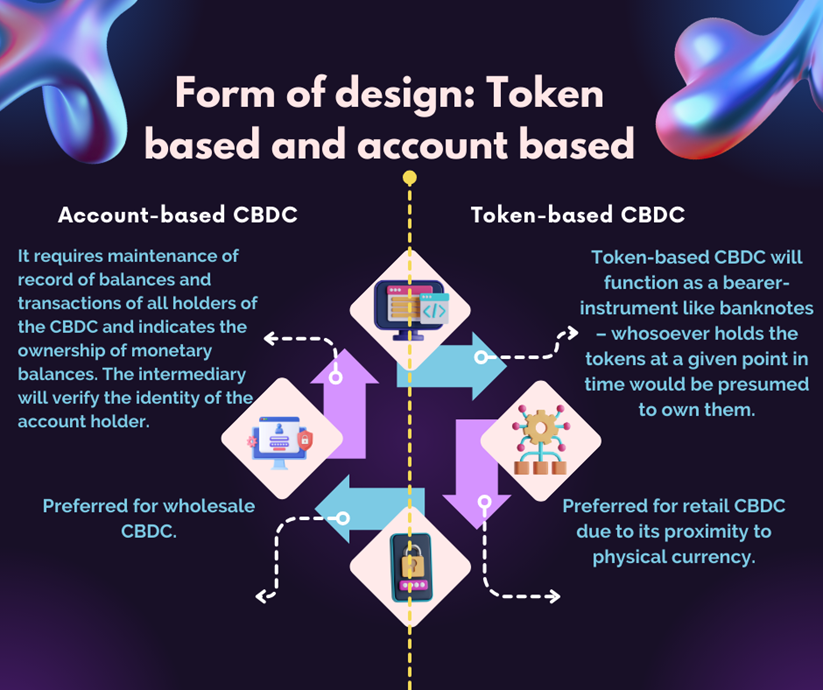

Form of CBDC: Deciding whether CBDCs will be Token-based or Account-based.

Instrument Design: Evaluating whether CBDCs should be Remunerated (earning interest) or Non-remunerated.

Degree of Anonymity: Considering the level of anonymity or privacy that users of CBDCs should have.

These design choices are pivotal in shaping how CBDCs will operate and integrate into the existing financial landscape, and they must be made thoughtfully to ensure a smooth transition and minimize disruptions.

In the following section, we will explore the primary reasons for the introduction of India’s central bank digital currency.

Key Motivations for the Introduction of Central Bank Digital Currency India

Central Bank Digital Currencies (CBDCs) offer unique advantages as sovereign currencies, including the trust, safety, liquidity, settlement finality, and integrity associated with central bank money. In India, the exploration of CBDC issuance is motivated by various factors.

These include reducing operational costs linked to managing physical cash, promoting financial inclusion, enhancing the resilience, efficiency, and innovation of the payment system, improving settlement system efficiency, fostering innovation in cross-border payments, and providing the public with the benefits that private virtual currencies offer without the associated risks. The offline feature of CBDC can be particularly valuable in remote areas, ensuring availability and resilience in situations where electrical power or mobile networks are unavailable.

Private virtual currencies represent a departure from the traditional concept of money, as they lack intrinsic value and are not backed by commodities. The rapid proliferation of private cryptocurrencies in recent years has challenged the conventional understanding of money. These cryptocurrencies claim the advantages of decentralization and are often viewed as innovations that could disrupt the traditional financial system. However, the design of cryptocurrencies is primarily aimed at circumventing established and regulated intermediaries and control mechanisms, which play a crucial role in maintaining the integrity and stability of the monetary and financial ecosystem.

As the guardian of the monetary policy framework and with a mandate to ensure financial stability, the Reserve Bank of India has consistently highlighted the various risks associated with cryptocurrencies. These digital assets can undermine the financial and macroeconomic stability of India, with negative consequences for the financial sector. Furthermore, the widespread adoption of cryptocurrencies could diminish the ability of monetary authorities to formulate and regulate monetary policy, posing a serious challenge to the stability of the country’s financial system.

In this context, it is the central bank’s responsibility to offer its citizens a risk-free form of central bank digital money. This will provide users with the same experience as dealing in digital currency, without the associated risks of private cryptocurrencies. Therefore, CBDCs will deliver the benefits of virtual currencies to the public while ensuring consumer protection and avoiding the adverse social and economic consequences associated with private virtual currencies.

Here let’s have a look at the benefits of issuance of CBDC in detail –

The adoption of Central Bank Digital Currencies (CBDCs) is motivated by a diverse set of reasons in different jurisdictions, including:

Popularizing Electronic Currency: In some countries like Sweden, where the usage of physical paper currency has been declining, the introduction of CBDC is seen as a way to promote a more widely accepted electronic form of currency.

Efficiency in Cash Issuance: In nations with significant physical cash usage such as Denmark, Germany, Japan, and the United States, CBDCs are considered to streamline the issuance process, making it more efficient.

Overcoming Geographical Barriers: In regions with geographical barriers, such as The Bahamas and the Caribbean, where islands are scattered, CBDCs can address the challenges related to the physical movement of cash.

Addressing Private Virtual Currencies: As private virtual currencies gain popularity, central banks aim to meet the public’s demand for digital currencies while avoiding the potential negative consequences associated with these private currencies.

Reduction in Cash Management Costs: The introduction of CBDC can lower the costs associated with managing physical cash, including expenses related to printing, storage, transportation, and replacement of banknotes.

Promotion of Digitization: CBDC can further the government’s goal of digitization, particularly in a case like India where despite rapid digitization, cash usage continues to rise. CBDC can redirect the preference for cash transactions towards digital payments.

Support for Competition, Efficiency, and Innovation: CBDC can enhance competition, efficiency, and innovation in the payments space, contributing to a diverse and resilient payment landscape. It provides another avenue for payments, particularly for e-commerce.

Improvement in Cross-Border Transactions: CBDCs have the potential to improve cross-border payments by offering faster, cheaper, and more transparent cross-border transactions. It can mitigate challenges related to time zones, exchange rate differences, and regulatory requirements.

Enhancing Financial Inclusion: CBDC can make financial services more accessible to the unbanked and underbanked populations, particularly in remote areas with limited infrastructure. It can also create digital financial records for easier access to credit.

Safeguarding Trust in the National Currency: In the face of the proliferation of cryptocurrencies, CBDCs can provide a risk-free, sovereign digital currency, ensuring the public’s trust in the national currency. It can also protect against the potential risks and volatility associated with private virtual currencies.

Features of Central Bank Digital Currency (CBDC)

CBDC is a sovereign currency issued by central banks to align with their monetary policy goals.

It is recorded as a liability on the central bank’s balance sheet.

CBDC is required to be universally accepted as a medium of payment, functioning as legal tender and a secure store of value for all citizens, businesses, and government entities.

It must be easily exchangeable with commercial bank money and physical cash.

CBDC is a fungible form of legal tender, allowing its use without the necessity of holding a bank account.

The implementation of CBDC is expected to reduce the costs associated with currency issuance and transaction processing.

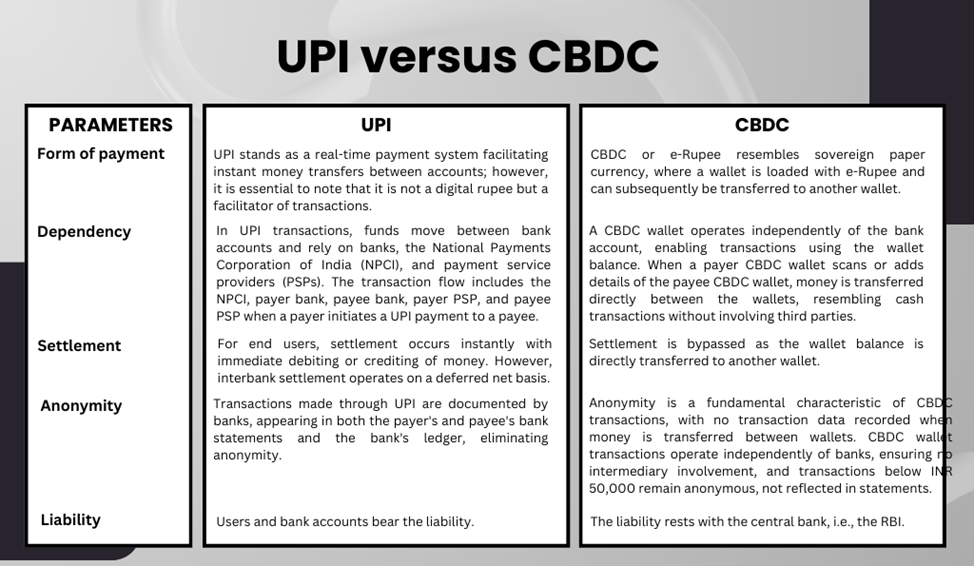

UPI versus CBDC

With the introduction of e-Rupee, there is uncertainty regarding the distinctions between UPI and CBDC. The table below clarifies these differences:

The Current worldwide situation regarding Central Bank Digital Currency (CBDC)

Over 60 central banks worldwide have shown interest in CBDC, including some that have already implemented it as either Retail or Wholesale CBDC. Others are exploring different frameworks, such as conducting research, testing, or launching CBDC.

The Bahamas, Jamaica, and Nigeria have successfully implemented CBDCs, with over 100 countries currently exploring this digital currency. Central bankers from Brazil, China, the euro area, India, and the United Kingdom are leading the way in these advancements.

17 other countries, including significant economies such as China and South Korea, are in the pilot stage and working towards launching their own central bank digital currency (CBDC). China was the first country to pilot their CBDC, known as e-CNY, in April 2022, with plans to expand its domestic use by 2023.

The increased adoption of central bank digital currency (CBDC) is viewed as a promising development and a significant advancement in the evolution of sovereign currency.

Several jurisdictions have approved the adoption of Central Bank Digital Currency (CBDC) for various reasons, some of which include –

The Central Banks encounter a shrink in the usage of paper currency with the objective of popularizing the electronic form of currency such as in Sweden.

The Central Banks pursue the requirement of the public with respect to digital currency to encourage the use of private virtual currencies. Hereto, evade damaging the consequences of private currencies.

The jurisdiction with the importance of physical cash usage in order to encourage efficient issuance, in countries such as the USA, Denmark, Japan.

The countries possessing geographical barriers that limit the physical movement of cash contains the motivation to use CBDC.

Development of Central Bank Digital Currency India

India’s CBDC architecture adopts the two-tiered model, widely used globally for CBDC implementations. In this model, banking intermediaries distribute CBDCs to the public based on the central bank’s provided MO supply. The interaction between central banks and commercial banks is facilitated by a hyperledger fabric. In the distribution tier, commercial banks and authorized intermediaries serve as nodes, transferring minted R-CBDC tokens from the central bank. The utilization and end-user interaction occur on an API-based framework, supported by an NPCI switch for routing interbank transactions.

India is one of the countries that is currently investigating the implementation of a central bank digital currency. In this blog section, we will discuss the latest updates on the digital rupee, also known as the central bank digital currency of India –

a. The First Pilot in The Digital Rupee India – Wholesale Segment (e₹-W)

The Indian government initiated the trial of the digital rupee RBI in the wholesale segment, starting on November 1st, 2022. The primary use case involves settling transactions in the secondary market for government securities. The e₹-W is expected to enhance the interbank market’s efficiency, and settling in Central Bank money will reduce transaction costs by eliminating the need for settlement guarantee infrastructure or collateral to manage settlement risks.

The RBI has selected nine banks to take part in the pilot project for Digital Rupee India wholesale –

Atomic swaps enhance settlement efficiency through automation.

2. Cross-Border Transactions Improvement:

Addresses challenges in high costs, low speed, and lack of transparency.

Accelerates settlement processes, overcoming time zone and exchange rate issues.

3. Money Market:

Facilitates trading in money markets like repo markets and interbank lending.

Enhances efficiency and transparency in pricing money market instruments.

Reduces counterparty risks and increases overall transparency.

B. Launch of First Pilot in The Digital Rupee India – Retail Segment (e₹-R)

The Reserve Bank of India (RBI) launched the first pilot of the Digital Rupee- Retail segment (e₹-R) on December 01, 2022.

The Hon’ble Minister of State for Finance Shri Pankaj Chaudhary announced that the pilot program for e₹-R is currently available in selected locations within a closed user group (CUG) consisting of participating customers and merchants. The five cities where the pilot program is available are Mumbai, New Delhi, Bengaluru, Bhubaneswar, and Chandigarh. e₹-R is a digital token that serves as legal tender, with the same denominations as paper currency and coins. It is being distributed through banks, acting as financial intermediaries. e₹-R provides the same trust, safety, and settlement finality as physical cash, but does not accrue interest and can be converted to other forms of money, such as bank deposits.

The Minister provided additional details and revealed that the RBI has picked eight banks to take part in the retail pilot project. These banks are the State Bank of India, ICICI Bank, Yes Bank, IDFC First Bank, Bank of Baroda, Union Bank of India, HDFC Bank, and Kotak Mahindra Bank. These banks have chosen specific individuals or account holders to participate in the trials.

A new e₹ wallet had been created specifically for the pilot program. This is because e₹ is a part of the currency system, while other digital wallets belong to the payments system. Users can use the e₹-R through a digital wallet provided by participating banks, which can be accessed on mobile devices.

The Reserve Bank of India (RBI) only releases a single digital currency called Central Bank Digital Currency (CBDC) on behalf of the Indian government. This currency is a liability of the Central Bank.

The e₹-R is a digital token that represents legal tender and comes in denominations similar to paper currency and coins currently in circulation. These tokens will be distributed through intermediaries, such as banks, and users will be able to transact with e₹-R using digital wallets provided by the banks. These wallets can be stored on mobile phones or other devices.

These transactions can be of both types, that is Person to Person (P2P) and Person to Merchant (P2M), the latter (Person to Merchant) can be done through QR codes displayed at merchant locations.

Additionally, the retail industry would include the important aspects of physical currency, such as trust, safety, and the assurance of final settlement.

Use in the Retail Segment:

1. Retail Cross-Border Remittances:

Cost reduction and increased speed and reliability.

Especially beneficial for migrant workers sending money to families in India.

2. Microfinance:

Supports small loans and savings through secure digital platforms.

Embeds features like programmability, alternative underwriting models, and digital onboarding.

3. Programmability:

Streamlines direct disbursal for widening financial inclusion.

4. Offline Payments:

Suited for offline transactions, crucial for reaching the last layer.

CBDCs, as tokens, enable offline payments.

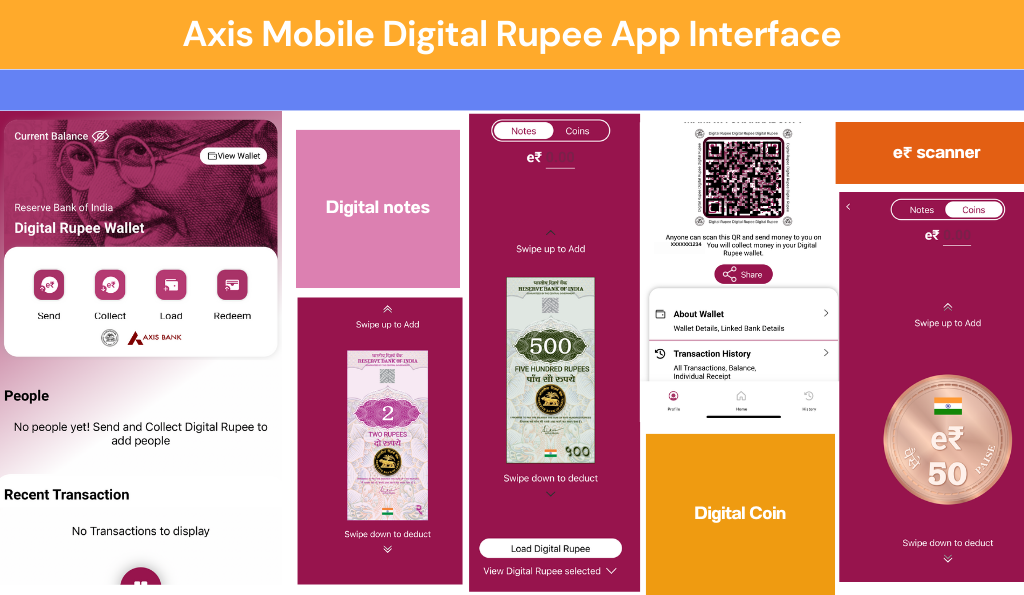

Empowering Transactions: Unveiling the Future of Digital Currency with the E-rupee App

Numerous banks have embraced the digital revolution by introducing dedicated e-rupee apps, catering to the evolving needs of their customers. Among the trailblazers in this transformative journey are notable banks such as State Bank of India (SBI), ICICI Bank, Kotak Mahindra Bank, Union Bank of India (UBI), Bank of Baroda, HDFC Bank, Canara Bank, Punjab National Bank (PNB), IDFC First Bank, IndusInd Bank, Axis Bank, Yes Bank, and Federal Bank.

These forward-thinking banks have recognized the significance of providing seamless, efficient, and secure digital currency services to their customers. The e-rupee apps serve as a gateway to a wide array of financial transactions, ranging from basic fund transfers to more complex activities like online payments, investment management, and digital currency exchanges. Users can experience the convenience of managing their finances at their fingertips, with the assurance of robust security measures implemented by these trusted banking institutions.

The advent of e-rupee apps marks a pivotal shift towards a cashless and digitally-driven economy, fostering financial inclusion and enhancing the overall banking experience for customers. With features such as real-time transaction tracking, personalized financial insights, and user-friendly interfaces, these apps aim to simplify the complexities associated with traditional banking processes. The competitive landscape among these banks further fuels innovation, with each institution striving to offer unique and value-added features to stay ahead in the dynamic digital financial services sector.

As these banking giants continue to invest in technology and user-centric solutions, the e-rupee apps not only signify a commitment to staying abreast of technological advancements but also reflect a dedication to providing unparalleled convenience and accessibility to customers in an increasingly digital era. The collaborative efforts of these banks contribute significantly to reshaping the landscape of banking services, making financial interactions more efficient, transparent, and tailored to the evolving needs of the modern-day consumer.

Here we are providing visual elements showcasing the distinct elements of e-rupee services of these banks. Through these visual cues, users can gain a firsthand glimpse into the innovative features and user interfaces that these banks offer within their respective e-rupee apps.

Key considerations for increasing adoption/ usage of CBDC

1. Policy Framework:

Anonymity:

Expectations of tiered anonymity with a transaction threshold.

Additional KYC for transactions beyond the threshold.

Data Privacy:

Strong, customized data privacy frameworks.

Prioritize citizens’ best interests and limit personally identifiable information.

2. Technology:

Scaling up Central Infrastructure:

Emphasis on modular DLT architecture for controllable decentralization.

Focus on increasing capacity with growing transactions and throughputs.

Operational Efficiency:

Expand operational capacity by setting distribution layer rules.

Let ecosystem players determine on-demand computing capacity.

3. Business Case:

Viable Business Case:

Define a viable business case, including typical and new CBDC features.

Incorporate features like programmability and offline capabilities.

Technology Enablers:

Open APIs play a key role in creating a level playing field.

Help ecosystem players innovate with supervised backend access.

Services:

Banks and non-banks build core value propositions for a CBDC portfolio.

Key areas include access-based services, user applications, e-wallets, processing support, and technology vendors.

The rollout of CBDC or e-Rupee marks a significant step in India’s digital transformation. With the recent phasing out of the INR 2,000 banknote, CBDC could become the ideal currency for trustworthy, resilient, and efficient financial transactions. Addressing potential implementation challenges, CBDC has the potential to enhance ease of doing business by overcoming geographical barriers. As cash usage declines, CBDC can provide stability, promote financial and environmental sustainability, foster financial inclusion, and catalyze innovation.

Key Takeaways

In conclusion, the introduction of the Digital Rupee, India’s Central Bank Digital Currency (CBDC), represents a significant milestone in the evolution of money and the payment landscape. This initiative aligns with the global trend of exploring and implementing CBDCs, with over 60 central banks around the world actively considering or implementing their own digital currencies.

The Digital Rupee is designed to combine the advantages of electronic payments, including enhanced efficiency, security, and financial inclusion, with the trust and stability that central bank-backed currency provides. It aims to promote digitization, streamline cash management, and offer the benefits of digital currencies without the associated risks of private cryptocurrencies.

Investment through Indian companies in foreign is a common phenomenon and several Indian companies have a presence in foreign companies by virtue of the formation of Joint Venture (JV) and Wholly Owned Subsidiaries (WOS). In contrast, Overseas Direct Investment by Indian residents has been revised to sanction overseas investment, with adequate manacles to prevent money from siphoning into foreign companies.

Justify Text Alignment

Therefore, adequate measures and regulations have been introduced and are being revised constantly to prevent any such event.

Reserve Bank of India (RBI) with effect from August 2022 has incorporated erstwhile FEMA (Transfer or Issue of Foreign Security) Regulations, 2004 and FEMA (Acquisition and Transfer of immovable property outside India) Regulation 1915 (OI Rules), which has introduced FEMA (Overseas Investment) Rules, 2022 (OI Regulation) and earlier regulations are considered superseded.

The FEMA (Overseas Investment) Directions, 2022 contains operational requirements under OI Rules and OI Regulations, including guidance regarding the interpretation, a grouping of conditions (under 3 categories, i.e., General provisions, Specific provisions, and Other operational instructions to AD banks).

In addition to that, it also contains particular compliance requirements from former ODI Master Directions and does not fall under OI rules and regulations.

With that, overseas investment in foreign is constricted unless completed in accordance with FEMA Act, OI Rules, and Regulations. This blog provides you with an overview of the latest notified and revised rules and regulations, including board amendments in RBI ODI.

India’s outbound investments have undergone a significant transformation, not only in terms of their scale but also in their geographical distribution and the sectors they target. Analyzing the trends in direct investments over the past decade reveals that while both inbound and outbound investment flows were relatively slow in the early part of the decade, they gained momentum in the latter half.

Over the last decade or so, there has been a noticeable shift in the destinations of overseas investments. In the first half, these investments were primarily focused on resource-rich nations like Australia, the United Arab Emirates (UAE), and Sudan. However, in the latter half, there was a shift towards nations offering greater tax advantages, such as Mauritius, Singapore, the British Virgin Islands, and the Netherlands.

Indian companies primarily engage in foreign investments through mergers and acquisitions (M&A). A developing country like India continually seeks opportunities to invest abroad as it contributes to the overall economy. These overseas investments by Indian companies also play a role in enhancing the performance of the country’s service and manufacturing sectors and contribute to addressing the challenge of rising unemployment rates. With the increasing M&A activity, companies gain direct access to new and broader markets, as well as advanced technologies, allowing them to expand their customer base and establish a global presence.

Overview of Amendments in RBI ODI

Investments made by individuals residing in India in foreign countries broaden the scale and range of business activities for Indian entrepreneurs. They offer global avenues for expansion, enabling easier access to technology, research and development resources, access to a broader global market, and lower capital costs. These advantages enhance the competitiveness of Indian businesses and contribute to the strengthening of their brand reputation.

Furthermore, such overseas investments serve as significant catalysts for foreign trade and the transfer of technology. This, in turn, leads to increased domestic employment, higher levels of investment, and overall economic growth through these interconnected relationships.

In alignment with the principles of liberalization and the facilitation of a more business-friendly environment, the Central Government and the Reserve Bank of India have undertaken a progressive simplification of procedures and a rationalization of rules and regulations governed by the Foreign Exchange Management Act, 1999. As a significant step in this direction, a new Overseas Investment framework has been put into operation.

The Central Government has issued the Foreign Exchange Management (Overseas Investment) Rules, 2022, through Notification No. G.S.R. 646(E) dated August 22, 2022, and the Reserve Bank of India has notified the Foreign Exchange Management (Overseas Investment) Regulations, 2022, under Notification No. FEMA 400/2022-RB dated August 22, 2022. These regulations supersede the previous Notification No. FEMA 120/2004-RB dated July 07, 2004 (Foreign Exchange Management – Transfer or Issue of any Foreign Security – Amendment – Regulations, 2004) and Notification No. FEMA 7 (R)/2015-RB dated January 21, 2016 (Foreign Exchange Management – Acquisition and Transfer of Immovable Property Outside India – Regulations, 2015).

The new framework simplifies the existing system for overseas investments by Indian residents, extending its coverage to a broader spectrum of economic activities, and substantially reducing the necessity for seeking specific approvals. This, in turn, will alleviate the burden of compliance and the associated compliance costs.

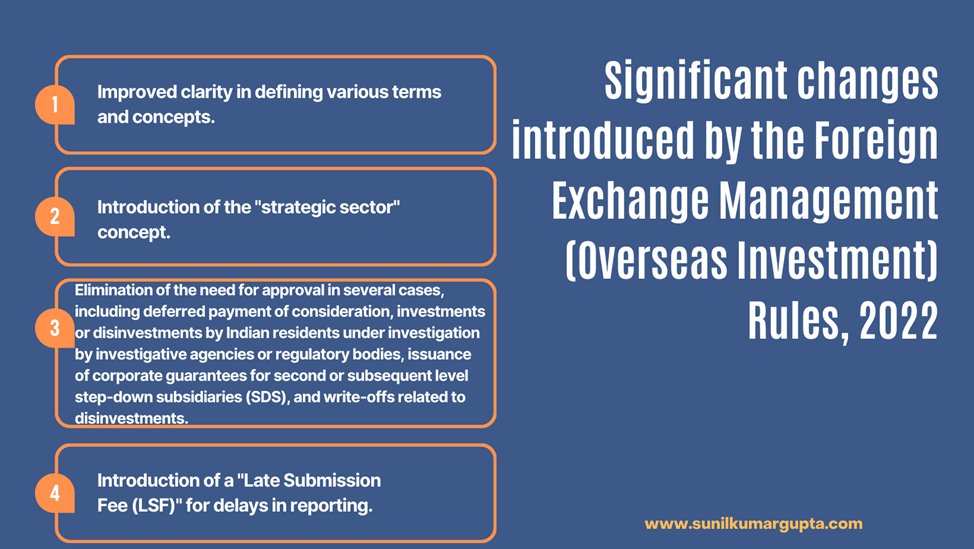

Some of the significant changes introduced by the new rules and regulations:

Improved clarity in defining various terms and concepts.

Introduction of the “strategic sector” concept.

Elimination of the need for approval in several cases, including deferred payment of consideration, investments or disinvestments by Indian residents under investigation by investigative agencies or regulatory bodies, issuance of corporate guarantees for second or subsequent level step-down subsidiaries (SDS), and write-offs related to disinvestments.

Introduction of a “Late Submission Fee (LSF)” for delays in reporting.

Permission for Initiating Overseas Investments:

An individual residing in India is allowed to make or transfer investments or financial commitments abroad under the general permission/automatic route, subject to the regulations outlined in the OI Rules, Regulations, and these guidelines. Consequently, overseas investments can be made in a foreign enterprise engaged in legitimate business activities, either directly or through second or subsequent-level step-down subsidiaries (SDS) or special-purpose vehicles (SPV).

To make the intended financial commitment, the person should complete Form FC as provided in the “Master Direction – Reporting under the Foreign Exchange Management Act, 1999,” supported by the necessary documents, and approach the designated authorized dealer (AD) bank to facilitate the investment or remittance.

In cases where approval is required, the applicant should approach their designated AD bank, which will then submit the proposal to the Reserve Bank of India (RBI) after conducting a thorough examination and providing specific recommendations. The designated AD bank, before forwarding the proposal, must submit relevant sections of Form FC in the online Overseas Investment Declaration (OID) application and include the transaction number generated by the application in their reference. The proposal should be accompanied by the following documents:

Background and brief details of the transaction.

Reason(s) for seeking approval mentioning the extant FEMA provisions.

Observations of the designated AD bank with respect to the following:

Prima facie viability of the foreign entity;

Benefits which may accrue to India through such investment;

Financial position and business track record of the Indian entity and the foreign entity;

Any other material observation.

Recommendations of the designated AD bank with confirmation that the applicant’s board resolution or resolution from an equivalent body, as applicable, for the proposed transaction(s) is in place.

Diagrammatic representation of the organisational structure indicating all the subsidiaries of the Indian entity horizontally and vertically with their stake (direct and indirect) and status (whether operating company or SPV).

Valuation certificate for the foreign entity (if applicable).

Other relevant documents properly numbered, indexed and flagged.

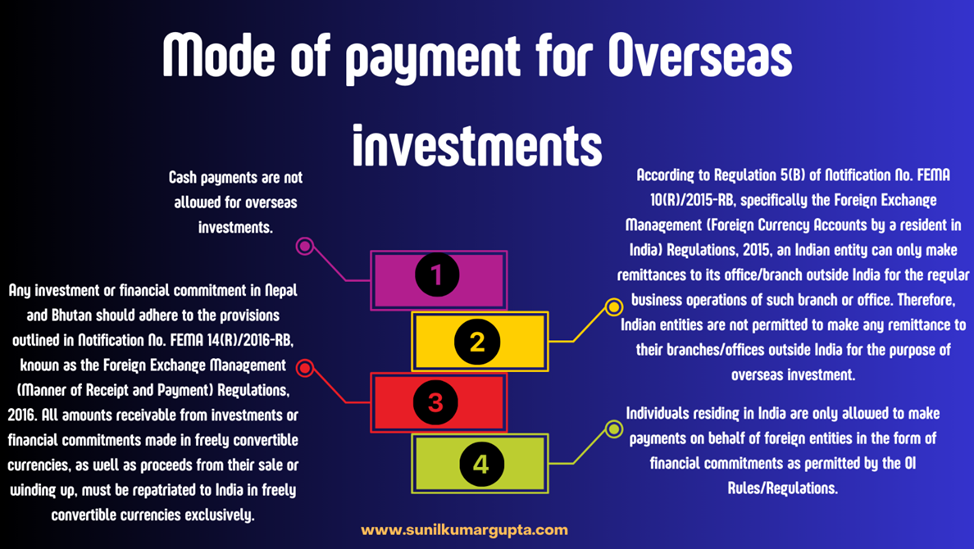

Mode of Payment

Regarding the method of payment for overseas investments made by an individual residing in India, the following provisions must be adhered to, as per regulation 8 of the OI Regulations. Additionally:

Pricing Guidelines

Before facilitating any transaction related to overseas investments, the Authorized Dealer (AD) bank must ensure compliance with the regulations specified in rule 16 of the OI Rules. Regarding the documents to be collected by the AD bank, they should adhere to a policy approved by their board, which should consider factors including valuation based on internationally accepted pricing methodologies. The AD bank is required to establish and implement a board-approved policy within two months from the date of issuance of these guidelines.

This policy can also address situations where valuation may not be mandatory, for instance, in cases involving transfers due to merger, amalgamation, demerger, or liquidation, where the price has been approved by a competent court or tribunal in accordance with Indian laws and/or the host jurisdiction. Another scenario could be when the price is readily available on a recognized stock exchange, and so on. The policy should also clearly specify additional documents, such as the audited financial statements of the foreign entity, which the AD banks may request to verify the legitimacy in cases where investments are being written off.

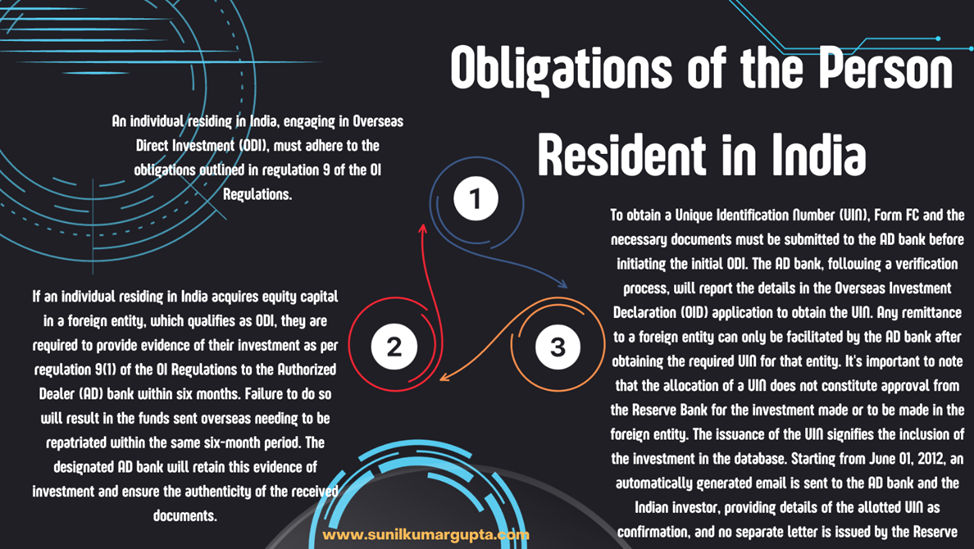

Obligations of the Person Resident in India

Reporting

All reporting related to overseas investments made by individuals residing in India should follow the guidelines specified in regulation 10 of the OI Regulations. This reporting should be done through the designated Authorized Dealer (AD) bank using the updated reporting forms and instructions outlined in the “Master Direction – Reporting under the Foreign Exchange Management Act, 1999.” The reporting forms can be downloaded from the Reserve Bank’s website at www.rbi.org.in. Any incomplete submissions will be treated as non-submissions.

Any acquisition of foreign securities resulting from the conversion of Indian Depository Receipts (IDRs) must be duly reported, either as Overseas Direct Investment (ODI) or Overseas Portfolio Investment (OPI), as applicable.

The Annual Performance Report (APR) should be certified by a chartered accountant in cases where statutory audits are not applicable, including for resident individuals. It’s important to note that in cases where APR is required to be jointly filed, one investor may be authorized by the other investors to submit the APR, or they may jointly file the report.

When a resident individual engages in overseas investments, they must adhere to the reporting requirements outlined in the OI Regulations. Additionally, reporting should also be carried out as per the Liberalized Remittance Scheme (LRS) guidelines when such investments are considered part of the LRS limit. It’s worth noting that the acquisition of foreign securities through inheritance or gift, in accordance with paragraph 2 of Schedule III of the OI Rules, is not counted against the LRS limit and, therefore, does not require reporting under the LRS.

Delay in Reporting

If an individual residing in India has experienced a delay in filing or submitting the necessary forms, returns, or documents, they have the option to file or submit these documents and pay the Late Submission Fee (LSF) through the designated Authorized Dealer (AD) bank, as specified in regulation 11 of the OI Regulations.

The Late Submission Fee (LSF) for delays in reporting transactions related to overseas investments will be calculated based on the following matrix:

Sr. No.

Type of Reporting delays

LSF Amount (INR)

1

Form ODI Part-II/ APR, FLA Returns, Form OPI, evidence of investment or any other return which does not capture flows or any other periodical reporting

7500

2

Form ODI-Part I, Form ODI-Part III, Form FC, or any other return which captures flows or returns which capture reporting of non-fund based transactions or any other transactional reporting

[7500 + (0.025% × A × n)]

Notes:

a) “n” is the number of years of delay in submission rounded-upwards to the nearest month and expressed up to 2 decimal points.

b) “A” is the amount involved in the delayed reporting.

c) LSF amount is per return.

d) Maximum LSF amount will be limited to 100 per cent of ‘A’ and will be rounded upwards to the nearest hundred.

e) Where an advice has been issued for payment of LSF and such LSF is not paid within 30 days, such advice shall be considered as null and void and any LSF received beyond this period shall not be accepted. If the applicant subsequently approaches for payment of LSF for the same delayed reporting, the date of receipt of such application shall be treated as the reference date for the purpose of calculation of LSF.

f) The option of LSF shall be available up to three years from the due date of reporting/submission under OI Regulations. The option of LSF shall also be available for delayed reporting/submissions under the Notification No. FEMA 120/2004-RB and earlier corresponding regulations, up to three years from the date of notification of OI Regulations.

g) In case a person resident in India responsible for submitting the evidence of investment or filing any forms/returns/reports, etc. as per OI Regulations/earlier corresponding regulations, neither makes such submission/filing within the specified time nor makes such submission/filing along with LSF as provided in regulation 11 of OI Regulations, such person shall be liable for penal action under the provisions of FEMA, 1999.

(3) The LSF may be paid by way of a demand draft drawn in favour of “Reserve Bank of India” and payable at the Regional Office concerned (in accordance with UIN mapping given in the table below).

Sr.No

UIN with prefix

UIN mapped to

1.

AH

RO Ahmedabad

2.

BG

RO Bengaluru

3.

BL or BY or PJ

RO Mumbai

4.

BN or CA or GA or GH

RO Kolkata

5.

CG or JM or JR or KA or ND or PT or WR

RO New Delhi

6.

HY

RO Hyderabad

7.

KO or MA

RO Chennai

Restrictions and prohibitions

Authorized Dealer (AD) banks are prohibited from facilitating transactions involving any foreign entity engaged in activities mentioned in rule 19(1) of the Overseas Investment (OI) Rules or located in countries/jurisdictions as advised by the Central Government under rule 9(2) of the OI Rules. It’s important to clarify that financial products linked to the Indian Rupee include non-deliverable trades related to foreign currency-INR exchange rates, as well as stock indices connected to the Indian market, among other things.

Individuals residing in India are not allowed to make financial commitments to a foreign entity that has invested or plans to invest in India at the time of such commitment or at any time thereafter, either directly or indirectly, resulting in a structure with more than two layers of subsidiaries. This restriction is in accordance with rule 19(3) of the OI Rules. It’s also specified that no additional layer of subsidiaries should be added to any structure that already has two or more layers of subsidiaries after the notification of the OI Rules/Regulations.

Please note that the term “subsidiary” is defined as an entity in which the foreign entity has control, which includes a stake of 10% or more in an entity, as per the OI Rules.

Financial commitment by an Indian entity

An Indian entity, subject to the overall limit specified in Schedule I of the Overseas Investment (OI) Rules and in compliance with Regulation 3 of the OI Regulations, is permitted to make financial commitments through Overseas Direct Investment (ODI) as outlined in Schedule I of the OI Rules, financial commitments through debt in accordance with Regulation 4 of the OI Regulations, and non-fund-based financial commitments in line with Regulations 5, 6, and 7 of the OI Regulations. Furthermore:

In cases of security swaps, both legs of the transaction must adhere to the provisions of the Foreign Exchange Management Act (FEMA), as applicable.

When a registered Partnership firm from India invests in a foreign entity, it is acceptable for individual partners to hold shares on behalf of the firm in the foreign entity, provided that the host country’s regulations or operational requirements necessitate such holdings.

Financial commitments through debt [Regulation 4 of the OI Regulations] – Authorized Dealer (AD) banks are authorized to facilitate outward remittances for financial commitments through debt only after obtaining the necessary agreements/documents to ensure the legitimacy of the transaction. An Indian entity is not allowed to lend directly to its overseas second or subsequent-level step-down subsidiary (SDS). Additionally, a resident individual cannot make financial commitments through debt.

Regarding financial commitments through Guarantees [Regulation 5 of the OI Regulations]:

In the case of performance guarantees, the specified time for contract completion is considered the validity period of the guarantee.