Financial activities of the Non-Banking Financial Companies (NBFCs) are regulated by Reserve Bank of India under the provisions of Chapter III B of the Reserve Bank of India Act, 1934. With the amendment of Section 45 IA of the Reserve Bank of India Act, 1934 in January 1997 and amendment of the National Housing Bank Act, 1987 in August 2019, in terms of Section 29 A of the National Housing Bank Act, 1987, all Non-Banking Financial Companies including Housing Finance Companies (HFCs) have to be mandatorily registered with the Reserve Bank of India.

Justify Text Alignment

Background

Consistent with the policy of giving greater operational freedom to banks in the matter of credit disbursement and in the context of mandatory registration of NBFCs with the Reserve Bank of India (RBI), most of the aspects relating to financing of NBFCs by banks have also been progressively deregulated. However, in view of the sensitivities attached to financing of certain types of activities undertaken by NBFCs, restrictions on financing of such activities continue to be in force.

Gist of the Master Circular

This Master Circular consolidates instructions on the above matter issued up to January 04, 2022 by which more autonomy have been given to NBFCs registered with RBI and is summarized hereunder:

The ceiling on bank credit linked to Net Owned Fund (NOF) of NBFCs has been withdrawn where NBFCs are engaged in principal business of asset financing, loan, factoring and investment activities. Accordingly, banks may extend need based working capital facilities and term loans to all NBFCs and engaged in infrastructure financing, equipment leasing, hire-purchase, loan, factoring and investment activities subject to provisions of para 8 of these guidelines.

Now, banks may also extend finance to NBFCs against second hand assets financed by them.

Banks may formulate suitable loan policy with the approval of their Boards of Directors within the existing/prudential guidelines and exposure norms prescribed by the Reserve Bank of India to extend various kinds of credit facilities to NBFCs.

Provision of financial assistance from Banks to Non-Banking Financial Companies (NBFCs) without Necessitating Registration

In terms of “Master Direction – Exemptions from the provisions of RBI Act, 1934” dated August 25, 2016,“ few categories of NBFCs are exempted from certain provisions of the RBI Act, 1934 including the need for registration with the RBI. Such NBFCs need not to register with the RBI and the banks may take their credit decisions on the basis of purpose of credit, nature, quality of underlying assets, repayment capacity of borrowers and risk perception, etc.

Activities not eligible for Bank Credit

(a.) The following activities undertaken by NBFCs are not eligible for bank credit:

(i) Bills discounted/rediscounted by NBFCs, except for rediscounting of bills discounted by NBFCs arising from sale of commercial vehicles and 2-wheeler and 3-wheeler vehicles subject to the following conditions:

the bills should have been drawn by the manufacturer on dealers only,

the bills should represent genuine sale transactions as may be ascertained from the chassis/engine number and

before rediscounting the bills, banks should satisfy themselves about the bonafides and track record of NBFCs which have discounted the bills.

(ii) Investments of NBFCs in any company/entity by way of shares, debentures, etc. However, need-based credit may be provided to Stock Broking Companies against shares and debentures held by them as stock-in-trade.

(iii) Unsecured loans/inter-corporate deposits by NBFCs to/in any company.

(iv) All types of loans and advances by NBFCs to their subsidiaries, group companies/entities.

(v) Finance to NBFCs for further lending to individuals for subscribing to Initial Public Offerings (IPOs) and for purchase of shares from secondary market.

(b.) Leased and Sub-Leased Assets

Banks can extend financial assistance to equipment leasing companies but they should not enter into lease agreements departmentally with such companies as well as other NBFCs engaged in equipment leasing.

Bank Finance to Factoring Companies

Banks can extendfinancial assistance to the Factoring Companies which comply with the following criteria with the restrictions mentioned at Paragraph 4.1 (i) and 4.1 (iv) above if:

(a) The companies qualify as Factoring Companies and carry out their business under the provisions of the Factoring Regulation Act, 2011 with notifications issued by RBI from time to time.

(b) They derive at least 50% of their income from factoring activity,

(c) The receivables purchased/ financed, irrespective of whether on ‘with recourse’ or ‘without recourse’ basis, form at least 50% of the assets of the Factoring Company ;

(d) The assets/ income referred to above would not include the assets/ income relating to any bill discounting facility extended by the Factoring Company,

(e) Credit limits extended by the Factoring Companies is secured by hypothecation or assignment of receivables in their favour.

Bank Finance to NBFCs not permitted for:

Bridge loans/interim finance

Banks should not grant bridge loans of any nature or interim finance against capital/debenture issues and/or in the form of loans of a bridging nature pending raising of long-term funds from the market by way of capital, deposits, etc. to all categories of NBFCs.

Advances against collateral security of shares to NBFCs

Shares and debentures cannot be accepted as collateral securities for secured loans granted to NBFC borrowers for any purpose.

Restriction on guarantees for placement of funds with NBFCs

Banks not to execute guarantees covering inter-company deposits/loans thereby guaranteeing refund of all type of deposits/loans accepted by NBFCs/firms from other NBFCs/firms. However, banks are permitted to provide Partial Credit Enhancement (PCE) to bonds issued by NBFC-ND-SIs and Housing Finance Companies (HFCs) as per guidelines contained at para 2.4 of the Master Circular on Guarantees and co-acceptances dated November 09, 2021 as updated from time to time.

Prudential ceilings for exposure of banks to NBFCs

(b.) Banks’ exposures to a single NBFC (excluding gold loan companies) will be restricted to 20 percent of their eligible capital base (Tier-I capital). However, based on the risk perception, more stringent exposure limits in respect of certain categories of NBFCs may be considered by banks. Banks’ exposures to a group of connected NBFCs or group of connected counterparties having NBFCs in the group will be restricted to 25% of their Tier-I Capital.

(c.) The exposure of a bank to a single NBFC which is predominantly engaged in lending against collateral of gold jewellery (i.e., such loans comprising 50% or more of their financial assets), shall not exceed 7.5% of the bank’s capital funds (Tier-I plus Tier-II Capital). However, this exposure ceiling may go up to 12.5% of banks’ Capital Funds if the additional exposure is on account of funds already lent by such NBFCs to the infrastructure.

(d.) Banks may also consider fixing internal limits for their aggregate exposure to all NBFCs put together.

(e.) Banks should have an internal sub-limit on their aggregate exposures to all NBFCs, having gold loans to the extent of 50% or more of their total financial assets, taken together. This sub-limit should be within the internal limit fixed by the banks for their aggregate exposure to all NBFCs put together as prescribed in paragraph 7.4 above.

(f.) Infusion of eligible Capital Funds, after the published balance sheet date, may also be taken into account for computing exposure ceiling subject to obtaining an external auditor’s certificate on completion of the augmentation of capital and its onward submission to RBI (Department of Supervision) before reckoning the additions to Capital Funds.

Restrictions regarding investments made by banks in securities/instruments issued by NBFCs:

(a.) Banks not to invest in Zero Coupon Bonds (ZCBs) issued by NBFCs unless the issuer NBFC builds up sinking fund for all accrued interest and keeps it invested in Government bonds.

(b.) Banks are permitted to also invest in Non-Convertible Debentures (NCDs) with original or initial maturity up to 1-year issued by NBFCs. However, while investing in such instruments, banks should be guided by the extant prudential guidelines in force, ensuring the disclosure of the purpose for which the NCDs are being issued in the disclosure document and such purposes are eligible for bank finance.

Conclusion

In view of policy measures to build scale and enhance NBFC’s contribution in

Global Trade significantly, RBI has brought the master circular, efforts have been made to ease financing to needy borrowers through NBFCs while sensitivities attached to financing have simultaneously been taken care of. We hope this masterstroke would definitely accelerate the trade and economic activity as is expected by Government of India.

Please also refer to previous Master Circular DBR.BP.BC.No.5/21.04.172/2015-16 dated July 1, 2015 on the captioned subject.

For more details on the topic, you may refer to Master Circular no RBI/2021-22/149/ DOR.CRE.REC. No.77/21.04.172/2021-22 dated January 05, 2022 of RBI or access the author at https://www.sunilkumargupta.com/ to explore more on other related topics.

During speech at the conference on 18th November, 2021 on ‘Creating synergies for seamless credit flow and economic growth’, our Prime Minister said “Indian banks are strong enough to play a major role in imparting fresh energy to the country’s economy, for giving a big push and making India self-reliant. I consider this phase as a major milestone in the banking sector of India”.

Justify Text Alignment

On this great occasion I wish to congratulate the Hon’ble Prime Minister on behalf of the industry, for suggesting various measures to commercial banks for easing out loan delivery process for providing better opportunities to business enterprises and start-ups. Our country’s outlook is now to intensify and spread the economic activities by providing hassle free loans to entrepreneurs. In the post Covid scenario, RBI’s role has to play an important role for boosting up economic activities and encouraging the banks to sanction loans at easy terms.

Prime Minister reiterated that banks have sufficient liquidity and coupled with the fact that now there is no backlog for provisioning of NPAs as NPAs in public sector banks are at the lowest compared to the five years back and this has led to upgrading of outlook for the Indian Banks by the International agencies. The Prime Minister said that apart from being a milestone, this phase is also a new starting point and called upon the banking sector to support the wealth creators and job creators. The Prime Minister empathetically said “It is the need of the hour for the banks of India to work proactively to bolster the wealth sheet of the country along with their balance sheets”.

PM urged bankers to identify the productive potential of citizens and go beyond the traditional banking when it comes to nourish their business intelligence and entrepreneurial dreams with quick release of loan funds. PM further stressed upon the need to go away with the feeling that lender is approver and customer is an applicant or receiver. Instead of waiting for the customers to come and seek loans, bankers have to come forward to analyse the credit appetite of both existing and potential customers and provide consultancy services with customized solutions and unified policies. In this way, banks have to adopt the model of partnership in which both partners share the benefits.

The Prime Minister said that due to recent implementation of various schemes, a huge pool of data is now available in the country. The Prime Minister emphasized that the banking sector must take advantage of this facility. He also listed the opportunities presented by the flagship schemes like PM Awas Yojana, Svamitva and Svanidhi and asked banks to participate and play their proactive role in these schemes.

Prime Minister said the scale at which corporates and startups are coming forward today is unprecedented and it is the opportune time to strengthen, fund, invest in India’s economic aspirations.

Some Highlights of Hon’ble PM’s Speech

Reduction In NPA

He quoted detailed reports while saying that NPA ratio of public sector banks has now come down to the lowest during last 5 years and they are flushed with liquidity. PM quoted that public sector banks have recovered around 5 lakh crores of bad loans during last years but such news did not make headlines in core media due to illegitimate activities of some defaulters.

Need For Massive Credit Push

Inspite of the current Covid situation, it is assumed that economy will recover at growth rate of 8.7% to 10.5% during current fiscal. This study sounds good but a massive credit push is essential for businesses to remain operational without hindrance and to expand to new horizons.

Studies have also found that growth rate of non-food bank credit has increased to 6.8% in September, 2021 as compared to 5.1% during same period last year. Industrial loans however have seen the growth of only 2.5%. CARE ratings also hint that weekly average (net) liquidity surplus in banking system grew from Rs.4.5 lakh crores at the end of June, 2021 to around Rs.7.5 lakh crores as of September-end.

Time For Action To Contribute to Economy

Bank’s participation in the growth of nation’s economy is undeniable. Banks maintain strict protocols while sanctioning loans. This exercise makes entrepreneurs to wait for long period and delay the process for unwanted reasons. Bankers must overlook traditional methods to approve loans.

PM assures the banks with dependable words and announced to provide all possible help. It is however important for loan seekers to maintain all records and provide all necessary documents for faster disbursal of loan funds.

Make Loan Dispensation Process Easy And Time Bound

He also appreciated the proposal to set up the web-based project funding tracker. This proposal will make all ministries and banks to work in tandem. PM also suggested adding this proposal as an interface to Gati Shakti Portal. Faster loan disbursal process will also help to effectively cope with other big challenges of unemployment and fund crunch.

In view of the abovementioned facts, it may be safe to conclude that the Government is fully committed to support Indian economy by promoting businesses and providing easy availability of funds through banks. It becomes pertinent for banks to be proactive in considering genuine loan requests and make sure that the funds sanctioned are being used only for the said purpose. Misuse of bank funds may land customer and/or concerned authorities into trouble and may attract various penal actions.

Non-Banking Financial Companies (NBFCs) have been growing in size and have substantial interconnectedness with other segments of the financial system. Reserve Bank of India had introduced a PromptCorrective Action Framework (PCA) for Scheduled Commercial Banks in 2002 and the same has been reviewed from time to time based on the experience gained and developments in the banking system. Accordingly, RBI has now decided to put in place a PCA Framework for NBFCs to initiate and implement remedial measures in a timely manner so as to restore its financial health for strengthening the supervisory tools applicable to NBFCs.

Justify Text Alignment

The PCA Framework for NBFCs, as summarized hereunder, comes into effect from October 1, 2022 based on the financial position of NBFCs on or after March 31, 2022. The objective of the PCA Framework is to enable supervisory intervention at appropriate time and is intended to act as a tool for effective market discipline. The PCA Framework does not preclude the Reserve Bank of India from taking any action as it deems fit at any time in addition to the corrective actions prescribed in the framework.

A. The PCA framework is applicable to the following category of NBFCs:

All Deposit Taking NBFCs [Excluding Government Companies] (NBFCs-D)

All Non-Deposit Taking NBFCs in Middle, Upper and Top Layers 3 (NBFCs-ND),

[Including Investment and Credit Companies, Core Investment Companies (CICs), Infrastructure Debt Funds, Infrastructure Finance Companies, Micro Finance Institutions and Factors]; but [Excluding – (i) NBFCs not accepting/not intending to accept public funds 4; (ii) Government Companies, (iii) Primary Dealers and (iv) Housing Finance Companies].

B. For NBFCs-D and NBFCs-ND, Capital and Asset Quality would be the key areas for monitoring in PCA framework. For CICs, Capital, Leverage and Asset Quality would be the key areas for monitoring in PCA framework.

C. For NBFCs-D and NBFCs-ND, indicators to be tracked would be Capital to Risk Weighted Assets Ratio (CRAR), Tier-I Capital Ratio and Net NPA Ratio (NNPA). For CICs, indicators to be tracked would be Adjusted Net Worth/Aggregate Risk Weighted Assets, Leverage Ratio and NNPA.

D. A NBFC will generally be placed under PCA framework based on the audited Annual Financial Results and/or the Supervisory Assessment made by the RBI. However, the RBI may impose PCA on any NBFC during the course of a year (including migration from one threshold to another) in case the circumstances so warrant.

E. The Reserve Bank of India may issue a press release when a NBFC is placed under PCA as well as when PCA is withdrawn vis-à-vis a NBFC.

F. Breach of any risk threshold may result in invocation of PCA as detailed under:

For NBFCs-D and NBFCs-ND (excluding CICs):

Indicator

Risk Threshold-1

Risk Threshold-2

Risk Threshold-3

CRAR

Up to 300 bps below the regulatory minimum CRAR [currently, CRAR <15% but ≥12%]

More than 300 bps but up to 600 bps below regulatory minimum CRAR [currently, CRAR <12% but ≥9%]

More than 600 bps below regulatory minimum CRAR [currently, CRAR <9%

Tier I Capital Ratio

Up to 200 bps below the regulatory minimum Tier-I Capital Ratio [currently, Tier-I Capital Ratio <10% but ≥8%]

More than 200 bps but up to 400 bps below the regulatory minimum Tier-I Capital Ratio [currently, Tier-I Capital Ratio <8% but ≥6%]

More than 400 bps below the regulatory minimum Tier-I Capital Ratio [currently, Tier-I Capital Ratio <6%]

NNPA Ratio (including NPIs)

>6% but ≤ 9%

>9% but ≤12%

>9% but ≤12%

For Core Investment Companies (CICs)

Indicator

Risk Threshold-1

Risk Threshold-2

Risk Threshold-3

Adjusted Net Worth/Aggregate Risk Weighted Assets

Up to 600 bps below the regulatory minimum ANW/RWA [currently, ANW/RWA <30% but ≥24%]

More than 600 bps but up to 1200 bps below regulatory minimum ANW/RWA [currently, ANW/RWA <24% but ≥18%]

More than 1200 bps below regulatory minimum ANW/RWA [currently, ANW/RWA <18%]

Leverage Ratio

≥2.5 times but <3 times

≥ 3 times but <3.5 times

≥3.5 times

NNPA Ratio (including NPIs)

>6% but ≤ 9%

>9% but ≤12%

>12%

G. Exit from PCA and withdrawal of restrictions under PCA – Once a NBFC is placed under PCA, taking the NBFC out of PCA framework and/or withdrawal of restrictions imposed under the PCA framework will be considered: a) if no breaches in risk thresholds in any of the parameters are observed as per four continuous quarterly financial statements one of which should be Annual Audited Financial Statement (subject to assessment by RBI), and b) based on supervisory comfort of the RBI including an assessment on sustainability of profitability of the NBFC.

H. The menu of corrective actions is as below:

Mandatory and Discretionary actions

Specifications

Mandatory actions

Discretionary actions

Risk Threshold – 1

1. Restriction on dividend distribution/remittance of profits,2. Promoters/shareholders to infuse equity and reduction in leverage,3. Restriction on issue of guarantees or taking on other contingent liabilities on behalf of group companies (only for CICs)

Common menuSpecial Supervisory ActionsStrategy RelatedGovernance RelatedCapital RelatedCredit Risk RelatedMarket Risk RelatedHR RelatedProfitability RelatedOperations/Business RelatedAny Other

Risk Threshold – 2

In addition to mandatory actions of threshold: Restriction on branch expansion

Risk Threshold – 3

In addition to mandatory actions of threshold 1 & 2,1. Appropriate restrictions on capital expenditure other than for technological upgradation within board approved limits2. Restrictions/reduction in variable operating costs

Common Menu for Selection of Discretionary Corrective Actions by the RBI are mentioned below:

Special Supervisory Actions

Strategy Related Actions

Governance Related Actions

Capital Related Actions

Credit Risk Related Actions

Market Risk Related Actions

HR Related Actions

Profitability Related Actions

Operations Related Actions

Any other specific action that the RBI may deem fit considering specific circumstances of the NBFC.

RBI would initiate suitable corrective actions including in particular mandatory and discretionary actions to check the wrong doings of the companies. Corrective measures are summarized in brief i.e. may conduct Special Supervisory Monitoring Meetings at quarterly or other identified frequency, special inspections/targeted scrutiny of the NBFC, restricted and need based regulatory/supervisory approvals, review short-term strategy, medium-term business plans, identify achievable targets and set concrete milestones for progress and achievement, may recommend to promoters/shareholders to remove and bring in new management/board, restriction in expansion of high risk-weighted assets, preparation of time bound plan and commitment for reduction of stock of NPAs, restrictions on branch expansion plans, PCAs would prove to be a milestone in the history of NBFCs and RBI will definitely have more control over NBFCs and would protect interest of the public funds at large.

For more details on the topic, you may refer to circular no RBI/2021-22/139DoS.CO.PPG. SEC.7/ 11.01.005/2021-22 dated Dec. 14, 2021 of RBI or access the author at: www.sunilkumargupta.com/ to explore more on other topics.

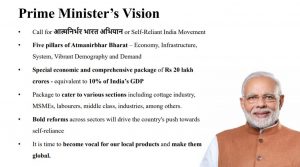

We congratulate our Hon’ble Prime Minister & Finance Minister for announcing the economic package in 5 parts to make India self-reliant (Aatmanirbhar Bharat) i.e., #AatmaNirbharBharat and for better opportunities for post-COVID-19. I am happy to share some points from my report published on 9th May 2020 on various social media platforms and where the Government was tagged, also found a place in the package like:

Release of pending payment of MSMEs from PSUs

Increasing the existing loan limit of the MSME sector by 20%, without any additional collateral securities

Creation of a digital market for MSMEs

Ease and deferment of labour law: Now, all occupations have been opened for women and permitted to work at night with safeguards. Major State Governments are now working on relaxing or deferring the labour law applicability

The Indian Government has always been reviewing its policies in the best interest of the country. The focus should now be drawn on improving India’s performance in ease of doing business by reviewing and rationalizing its policies in Dealing with Construction Permits, Getting Electricity, Registering Property, Paying Taxes, Trading across Borders, Enforcing Contracts, Resolving Insolvency, Employing Workers and Contracting with the Government. The government has started working on ease of doing business relating to easy registration of property and fast disposal of commercial disputes for making India one of the easiest places to do business as a part of the next phase of Ease of Doing Business Reforms.

Ease of Corporate Law and IBC laws to enhance businesses and to believe in entrepreneurs

De-punitive and de-criminalisation of corporate and business laws: a) lower penalties for all defaults for Small Companies, One person Companies, Producer Companies & Start-Ups. b) decriminalization of Companies Act violations involving minor technical and procedural defaults (shortcomings in CSR reporting, inadequacies in board reports, filing defaults, delay in holding AGM). c) majority of the compoundable offences sections are to be shifted to internal adjudication mechanism (IAM) and powers of RD for compounding enhanced (58 sections to be dealt with under IAM as compared to 18 earlier). d) 7 compoundable offences altogether dropped and 5 to be dealt with under an alternative framework

All these will enable businesses to complete their pending compliances without payment of any additional filing fees, thereby the entrepreneurs may focus on the growth of their businesses and simultaneously de-clog the criminal courts and NCLT.

The whole world is struggling hard with the global lockdown during the pandemic COVID-19 and is striving its best to regain its economies. The IMF World Economic Outlook came out with its interesting growth projections stating that the Euro Area is projected to have a de-growth in 2020 at minus 7.5% and projected growth of 4.7% in 2021. They have projected that India will have a better position by attaining 1.9% in 2020 and 7.4% in 2021 as against a contraction in the global economy. India has great opportunity to become a global manufacturing hub and to boost their MSME sector which is the lifeline of the country which eventually contributes 45% of the total manufacturing and 40% of the total exports and provides huge employment to all the skilled, semiskilled and unskilled youth of the country.

Justify Text Alignment

The pandemic COVID-19 had its origin in China and it has gradually spread its claws all over the world creating global economic destruction and resulting in Anti-Chinese sentiments in the system. Now businesses and manufacturers are looking for possible alternative locations to set up their manufacturing units. Various companies are planning to shift its manufacturing units from China to India, Vietnam, Thailand, Indonesia, Eastern Europe etc. India is being seen as a viable option to become a global manufacturing destination going forward. Countries like Japan are in talk with the Indian Government to set up their base in India. Market giants like Pegatron Corp., Google, Microsoft, Apple’s manufacturing partner Wistron Corporation are planning to move out of China and set up their manufacturing units in countries like India, Vietnam, Thailand, Indonesia etc. India is one of the good choices for these companies due to its young population, availability of abundant land, skilled labour, low tax rate for new manufacturing units and favorable business environment. As per the World Bank latest 2019 data, in ease of doing business, Thailand ranks at 21, followed by India at 63, Vietnam at 70 and Indonesia at 73.

But is this all that is needed?

The entire world now is rethinking to develop their manufacturing niche in their own country or set up their manufacturing unit in any other country except China so as to avoid such devastating loss in the future. This is a brilliant opportunity for India to become the manufacturing hub of the world by pressing the reboot key to start afresh with new ideas and new goals in New India. Hence, it is important to justify why the businesses will shift to India and not to the other countries. Developing India as a manufacturing hub and an economic powerhouse is not like pressing the F5 key on the computer. Not only we have to attract the foreign companies to set up their manufacturing units in India, but also rejuvenate our MSME sector to grow and support our economy and the international manufacturing in India.

Let us now analyze whether doing business in India is really easy as compared to other nations. As per the World Bank study, there are majorly 12 indicators, whose aggregate score, giving equal weight to each indicator, determines the rankings of the countries in ease of doing business and they keep on changing on year to year basis.

Source: The World Bank

India is one among the top 10 countries which has shown major improvement in 2019 vis-à-vis 2018. After climbing up the ladder, due to business-friendly policies of Modi Government, India is now at 63rd position out of 190 countries with DB Score of 71.0 out of 100 points. These are the 10 indicators of ease of doing business which is prepared by comparing the business regulation in 190 countries and are being considered by the businesses (domestic and international) before starting a new venture:

Sl. No

Indicators

India

Way forward for better ranking by India

1

Starting a Business: This topic measures the number of procedures, time, cost and paid-in minimum capital requirement for a small- to medium-size business to start up and formally operate in each economy’s largest business city.

136

136 out of 190 is not a good score, we need to at least reach a score within 50 as far as starting a business is concerned. Norms for starting a new business needs to be relaxed and should be made online in time bound manner. Due to the federal structure and the nature of businesses, they has to take several permissions from the Central and State Governments. Thus, a close coordination should be there between both the governments. Though the Ministry of Corporate Affairs has already implemented various steps like reduction of fees for incorporation of Company, introduction of SPICe, formation of a Company in 1 day, relaxation in the minimum paid-up capital requirement for ease of doing business, but we have to review various other compliances applicable for starting a new business and try to reduce the number of procedures, time and cost of the entire process.

2

Dealing with Construction Permits: It tracks the procedures, time and cost for obtaining the necessary licenses and permits, submitting all required notifications, requesting and receiving all necessary inspections and obtaining all requisite connections and permissions.

27

India was at the 52nd position in 2018 as against 27th in 2019. Although India has streamlined the process and improved its quality building controls, with faster and less expensive procedures to get construction permits in Delhi and Mumbai, but for better ranks it is advisable to encourage digitalisation and online approval for easy operation by each of the State Governments. For a better ranking post lockdown, India should now reduce/ minimise the number of procedures for getting the construction permits along with the time and cost of the process and build more effective quality control parameters.

3

Getting Electricity: This indicates procedures, time and cost required for a business to obtain a permanent electricity connection.

22

Though we have reached a score of 22 out of 190, but we need to improve the score further. Automated mechanism needs to be set up for supply of electricity connection. Further, more solar and hydro power plants, transmission lines needs to be set up all across the country so that there is no scarcity of supply of electricity. Our country needs to focus on reducing the time, cost and number of procedures for getting the electricity connections and emphasise on reliability of supply and transparency of tariff.

4

Registering Property: This is one of the primary steps for any new business to set up. It examines the steps, time, and cost involved in registering an undisputed property i.e. land and/ land along with building.

154

We are at 154th position out of 190 countries, hence we need significant improvement in getting property registered in the name of businesses because owning a land/ property for businesses is one of the most important and critical steps in setting up a new business, wherein there are some improvements. The Government needs to rationalise the land acquisition law and standardise online system of allotment of land by the industrial development authorities. It is also required to work on increasing the quality of land and administration process along with better transparency and reduce/ minimise the time taken, cost and number of procedures.

5

Getting Credit: This topic covers two aspects of access to finance—the strength of credit reporting systems and the effectiveness of collateral and bankruptcy laws in facilitating lending.

25

The entire process of getting credit in India needs to be reviewed, relaxed, standardised and made online. The Government needs to strengthen the legal rights of all the parties in the contract as well as transparency in assessing the credit score and expand the scope of information collection and reported by credit bureau.

6

Protecting Minority Investors: It measures the strength of minority shareholder protections against misuse of corporate assets by directors for their personal gain as well as shareholder rights, governance safeguards and corporate transparency requirements that reduce the risk of abuse.

13

The interests of the minority investors needs to be protected more strictly. Disclosures needs to clearly explain the facts, terms and risks involved, extent of directors’ liability and shareholders rights should be highlighted. Policies for corporate transparency, ownership and control measures needs to be reviewed and rationalised.

7

Paying Taxes: It records the taxes and mandatory contributions that a medium-size company must pay or withhold in a given year, as well as the administrative burden of paying taxes and contributions.

115

India has a rank of 115 out of 190, which shows that the Government needs to review its taxation policies and significantly work on getting a better score within top 50. The Government needs to encourage businesses and individuals to pay tax and rationalise their compliances and administrative burden of collection should be bare minimum. They need to work on increasing total tax and contributions received and reduce the tax rates. Computation, compliance, filing and refund of direct and indirect taxes should be made easy. The taxation system needs to be made uniform so that the taxpayers find it easy and just, to pay the taxes and the tax audit processes needs to be reviewed along with rationalising labour taxes and other mandatory contribution (other than tax on profit).

8

Trading across Borders: Doing Business records the time and cost associated with the logistical process of exporting and importing goods. It measures the time and cost (excluding tariffs) associated with three sets of procedures—documentary compliance, border compliance and domestic transport—within the overall process of exporting or importing a shipment of goods.

68

India has implemented post clearance audits, integrating trade stakeholders in a single electronic platform, upgrading port infrastructures and enhancing electronic submission of documents in Delhi and Mumbai. The Government should now relax the existing laws regulating trade relations between India and other countries except the countries sharing land borders with India. While exporting or importing we have to reduce the time and cost for documentary compliance and border compliance.

9

Enforcing Contracts: It measures the time and cost for resolving a commercial dispute through a local first-instance court, and the quality of judicial processes index, evaluating whether each economy has adopted a series of good practices that promote quality and efficiency in the court system.

163

Since India now ranks at 163rd position out of 190 countries as per the World Bank data, the Government needs to stress on putting extra efforts in its system to enforce contracts. India Government should now bring out effective steps to resolve commercial disputes and enforce contracts. The Government should reduce the time to enforce contracts i.e. from the date of filing of dispute till the date of passing the order at the first-instance court with a minimum cost and increase the quality of judicial processes.

10

Resolving Insolvency: These variables are used to calculate the recovery rate, which is recorded as cents on the dollar recovered by secured creditors through reorganization, liquidation or debt enforcement (foreclosure or receivership) proceedings.

52

After the Insolvency laws, India has made resolving insolvency in a much easier way by promoting existing reorganisation proceedings. Government now needs to work on the effective implementation of the law in line with the international laws. Focus needs to be also drawn in increasing the recovery rate and strengthening the insolvency framework.

11

Employing workers: Labour laws to avoid worker exploitation, discrimination of hiring and working policies and unfair dismissal practices vis-à-vis rational and flexible labour laws for the growth of business

Not considered in ranking in 2019

The employing workers indicator measures regulation in the areas of hiring, working hours, and redundancy. A country should have flexible labour regulations, which provides workers an opportunity to choose their jobs and work freely, thereby increasing the labour productivity. India should have easy hiring framework with flexible rules so as to reduce the rate of unemployment among youth and female workers.

12

Contracting with the Government: Efficiency in public procurement policy to ensure better use of taxpayer’s money

Not considered in ranking in 2019

The contracting with the government indicator captures the time and procedures to win a public procurement contract. The Indian Government should review and take effective steps to prepare a database which constitutes a repository of comparable data on how efficiently public procurement processes are carried out and which will act as a benchmark to analyze efficiency of the entire public procurement life cycle. The procurement process should be an open unrestricted and competitive public call.

We have seen that since the past few years, India is significantly improving its position in ease of doing business as per the World Bank ranking. Apart from ease of doing, the country has to take some bold steps to come out of COVID-19 setback and achieve its dream of becoming the most attractive manufacturing hub and in establishing new businesses.

The biggest challenge for us is to create a lucrative environment for the international businesses by relaxing the compliance procedures followed in the country. The Government shall start easing the punitive and criminality clauses from compliance, business, commercial and labour laws and trusting the businesses so that the investors/businesses can concentrate more on the growth of their business, rather than wasting time on the compliance burdens. Government should rely on the self-declarations being given by the businesses and give them a more work friendly environment. Maximum companies prior to investing in India will compare the entry procedures i.e. starting a business in India, getting lands, enforcing contracts, statutory compliances, penalty and prosecution clauses in compliance, business and labour laws with that prevailing in other countries. The India Government is now focusing on interacting with the businesses and stakeholders of various other countries to set up their manufacturing base in India but the Central and State Governments may set up specific workforce for interacting with the foreign and Indian entrepreneurs and frame guidelines for timely completion of the projects. The said workforce may be formed jointly by the industry experts, professionals and Government representatives;

As a matter of continuous endeavor of the Government to promote MSME, enough safeguards are already built in the MSME law which states that for every services/goods supplied by the MSME unit, the buyer needs to make payment as per the pre-set terms but not exceeding 45 days and in case of delay, interest is charged. The Government needs to implement this law strictly and ensure that the dues from the State/ Central Government, PSUs and big corporates are paid to the MSMEs immediately along with the applicable interest. As per the law, MSME registration is very simple through Udyog Aadhaar (https://www.msmeregistration.org), however still a lot of MSMEs are unregistered and not able to get all the benefits allowed to registered MSMEs. The Government needs to ensure that all the MSMEs get themselves registered through the website. The State Governments should also relax or defer the labour law applicability on MSME sector for few years;

The Reserve Bank of India (RBI) needs to pump in more funds in the system to fund the MSME sector. The total liquidity injected in the market by RBI values 3.2% of the GDP, which the Government needs to ensure that it flows into the MSME sector. In order to fight the financial crisis caused by the COVID-19, the MSME sector may be granted a moratorium period of 6 months instead of 3 months and immediate fresh business loan may be granted to those MSMEs who do not have any existing loan. The cash flows of the MSMEs may be maintained by enhancing the overdraft limit to 25% without any primary security or otherwise, with repayment schedule starting after 6 months from the date of granting the facility. Further, the Government should strictly implement the ‘Credit Guarantee Fund Scheme’ to make available collateral-free credit upto Rs 2 crore to the micro and small enterprise sector. The Government should also ensure that the banks approve the loan to the MSMEs and the purpose of bringing this scheme doesn’t get defeated. The Government should also relax the norms pertaining to non-performing assets of the MSMEs to release the burden from their shoulders. They should further assure the banks/ financial institutions that in case any loan turns bad in future, the sanctioning authority will not be held liable and they will not be booked by the criminal law;

The State Governments has to promote MSMEs in manufacturing and service sectors in B-class, C-class, small towns and villages and link them with digital platforms for procuring raw materials and selling their goods. Though we have a few digital platforms for selling of goods in MSME sector which are run by the Government, but we need such digital platforms which will be run and managed by the MSMEs only and which can be operated in the local language also for easy understanding by the MSMEs.

The country’s agriculture sector accounts for 17% contribution in the GDP and has a growth rate of 2.1%. Out of the 138 cr population, approx. 58% population of the country is engaged in the agriculture sector. Since agriculture sector is the prime sector employing the maximum population of India, the Government needs to focus on increasing the percentage of the contribution to GDP from this sector by allowing businesses to invest in this sector by way of PPP model. Accordingly, the businesses can invest at the initial stages i.e. funding the farmer for seeds, fertilizer, labour cost etc. and purchase the entire crop at a price not which is being fixed by the Government. In case of any natural calamity or unforeseen circumstances resulting in loss of crop, the farmers and businesses should get the minimum fixed amount from the insurance company. The businesses may adopt this as their business model. Currently the Government through banks, provides loans to the farmers and if due to some natural calamity or otherwise, the crops get affected, then as a result of various compulsions, the Government has to waive off the loans and it creates a habit of financial indiscipline in the country.

Conclusion:

In this global crisis, each and every country is trying to start afresh and revive back its economic growth and become the new economic powerhouse. The Indian Government has always been reviewing its policies in the best interest of the country. The focus should now be drawn on improving India’s performance in ease of doing business by reviewing and rationalizing its policies in Dealing with Construction Permits, Getting Electricity, Registering Property, Paying Taxes, Trading across Borders, Enforcing Contracts, Resolving Insolvency, Employing Workers and Contracting with the Government. The existing punitive and criminality clauses from compliance, business, commercial and labour laws need to be reviewed and relaxed. Entrepreneurs and foreign businesses should be given a free hand to focus on the business growth and in turn aid in the economic growth of the country.

MSME sector is growing at 10%, which needs to be escalated by establishing MSME in small town and villages and connect them through digital platforms owned and run by the MSME sector in the local language also. The State Governments should relax or defer the labour law applicability on MSME sector and incentivise them link with their production for the next few years. The Government should strictly implement the ‘Credit Guarantee Fund Scheme’ to make available collateral-free credit upto Rs 2 crore to the MSME sector. They should also ensure that the banks approve the loan to the MSMEs and the purpose of bringing this scheme doesn’t get defeated. The Government shall also focus on developing the agricultural sector by allowing investment through farmer-business-government model where Government needs to allow investment by businesses and the minimum price should be controlled by the Government.